FORM NO. 10B

Accountant † Notes : 1. *Strike out whichever is not applicable. 2. †This report has to be given by- (i) a chartered accountant within the meaning of the Chartered Accountants Act, 1949 (38 of 1949); or (ii) any person who, in relation to any State, …

Download FORM NO. 10B

Information

Domain:

Source:

Link to this page:

Documents from same domain

Income from House Property - Income Tax …

www.incometaxindia.gov.inHouse I: As the house property is let out through out the previous year the annual value shall be determined as per . clauses (a) and (b) of Sec. 23(1)

Citizen's Charter - Declaration - Income Tax …

www.incometaxindia.gov.inc A DECLARATION OF OUR COMMITMENT TO THE TAXPAYERS INCOME DEPARTMENT GOVERNMENT OF INDIA 2014 The Citizen's Charter of the Income Tax Department is a declaration of its Vision, Mission and Standards of Service Delivery

TAX ON LONG-TERM CAPITAL GAINS - Income Tax …

www.incometaxindia.gov.in[As amended by Finance Act, 2018] TAX ON LONG-TERM CAPITAL GAINS Introduction Gain arising on transfer of capital asset is charged to tax under the head “Capital Gains”.

GOVERNMENT OF INDIA CENTRAL BOARD OF …

www.incometaxindia.gov.inCIRCULAR NO : 29 /2017 F.No. 275/192/2017-IT(B) Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes ***** North Block, New Delhi

Circular No.6/2016 Government of India - Central …

www.incometaxindia.gov.inCircular No.6/2016 Government of India MinistryofFinance Department ofRevenue Central Board ofDirectTaxes North Block, New Delhi, the 29th ofFebruary, 2016 Sub: Issue of taxability of surplus on sale of shares and securities - Capital Gains or Business

GOVERNMENT OF INDIA MINISTRY OF FINANCE …

www.incometaxindia.gov.inCIRCULAR NO : 01/2017 F.No. 275/192/2016-IT(B) Government of India Ministry of Finance Department of Revenue Central Board of …

NOTIFICATION - incometaxindia.gov.in

www.incometaxindia.gov.in[Notification No.16/2018/ F.No.370142/1/2018-TPL] (Dr. T.S. Mapwal) Under Secretary to the Government of India Note.-The principal rules were published in the Gazette of India, Extraordinary, Part-II, Section 3,

INDIAN INCOME TAX RETURN Assessment Year ITR …

www.incometaxindia.gov.inPage 1of 3 FORM ITR-2 INDIAN INCOME TAX RETURN [For Individuals and HUFs not having Income from Business or Profession] 2 (Please see Rule 12 of the Income …

![FORM NO. 3CA [See rule 6G(1)(a)] Audit report …](/cache/preview/5/e/9/7/6/b/7/4/thumb-5e976b74d05a63207c471fc48a86f3e5.jpg)

FORM NO. 3CA [See rule 6G(1)(a)] Audit report …

www.incometaxindia.gov.inFORM NO. 3CA [See rule 6G(1)(a)] Audit report under section 44AB of the Income -tax Act, 1961, in a case where the accounts of the business or profession of a person

TDS ON SALARIES - Income Tax Department

www.incometaxindia.gov.inINCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 TDS ON SALARIES Tax Payers Information Series - 35

Related documents

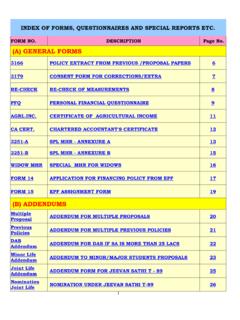

(A) GENERAL FORMS

www.joinlic.netchartered accountant's certificate 12 3251-a spl mhr - annexure a 13 3251-b spl mhr - annexure b 15 widow mhr special mhr for widows 16 form 14 application for financing policy from epf 17 form 15 epf assignment form 19 (b) addendums multiple …

Handbook on Certification of Form CSR - 1

csr.icai.orgMay 02, 2021 · Form CSR -1 is to be certified by a Chartered Accountant / Company Secretary / Cost Accountant. Therefore, a need was felt to guide the members on the requirements for verifying and certifying Form CSR-1. This Handbook on Certification of Form CSR-1 is an effort towards the same. I am thankful to CA. Atul Kumar Gupta, President and CA.

General Circular No. 36/2011 F. No. 2/3/2011-CL V ...

www.mca.gov.inAnnexure C, prepared as on date not prior to more than one month preceding the date of filing of application in Form FTE, duly certified by a statutory auditor or Chartered Accountant in whole time practice, as the case may be. (p) In the case of 100% Government companies, if no Board is in

CRITICAL ANALYSIS OF CLAUSE 34 OF FORM 3CD

www.voiceofca.inAnalysis of Form no. 26A: Annexure ZA [Certificate of accountant under first proviso to Section 201(1) of the Income Tax Act, 1961 for certifying the furnishing of return of income, payment of tax etc by the payee The following details are furnished in Annexure – ‘A’: