Transcription of 8594 Asset Acquisition Statement - 2013 Tax & …

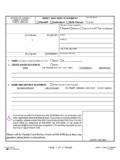

1 2 INSTRUCTIONS TO PRINTERSFORM 8594 , PAGE 1 of 2 MARGINS: TOP1 2", CENTER : HEAD TO HEADPAPER: WHITE WRITING, SUB. : BLACKFLAT SIZE: 17" x 11"FOLD TO: 81 2" x 11" PERFORATE: (ON FOLD)OMB No. 1545-1021 Asset Acquisition Statement8594 FormUnder Section 1060(Rev. February 2006)Department of the TreasuryInternal Revenue ServiceAttachmentSequence No. 61 Attach to your income tax as shown on returnSellerCheck the box that identifies you:1 Name of other party to the transactionOther party s identifying numberAddress (number, street, and room or suite no.)City or town, state, and ZIP codeForm8594(Rev.)

2 2-2006)For Paperwork Reduction Act Notice, see separate No. SPECIFICATIONSTO BE REMOVED BEFORE PRINTINGDO NOT PRINT DO NOT PRINT DO NOT PRINT DO NOT PRINTTLS, have youtransmitted all Rtext files for thiscycle update?DateActionRevised to printPurchaserIdentifying number as shown on returnGeneral Information2 Date of sale3 Total sales price (consideration)Part IPart IIOriginal Statement of Assets TransferredAllocation of sales priceAggregate fair market value (actual amount for Class I)Assets4$$Class I$$Class IIClass V$$To t a l$Did the purchaser and seller provide for an allocation of the sales price in the sales contract or in anotherwritten document signed by both parties?

3 5 NoYe sIf Yes, are the aggregate fair market values (FMV) listed for each of Asset Classes I, II, III, IV, V, VI, andVII the amounts agreed upon in your sales contract or in a separate written document?Ye sN oIn the purchase of the group of assets (or stock), did the purchaser also purchase a license or a covenantnot to compete, or enter into a lease agreement, employment contract, management contract, or similararrangement with the seller (or managers, directors, owners, or employees of the seller)?6 NoYe sIf Yes, attach a schedule that specifies (a) the type of agreement and (b) the maximum amount ofconsideration (not including interest) paid or to be paid under the agreement.

4 See instructions.$$$Class IV$$Class VI and VII$$Class III See separate TO PRINTERSFORM 8594 , PAGE 2 of 2 MARGINS: TOP1 2", CENTER : HEAD TO HEADPAPER: WHITE WRITING, SUB. : BLACKFLAT SIZE: 17" x 11" FOLD TO: 81 2" x 11"PERFORATE: (ON FOLD)Page2 Form 8594 (Rev. 2-2006)Supplemental Statement Complete only if amending an original Statement or previously filedsupplemental Statement because of an increase or decrease in consideration. See of sales price as previously reportedRedetermined allocation of sales priceIncrease or (decrease)Assets8 Class I$$$Class II$$$Class III$$$$To t a lReason(s) for increase or decrease.

5 Attach additional sheets if more space is year and tax return form number with which the original Form 8594 and any supplemental statements were SPECIFICATIONSTO BE REMOVED BEFORE PRINTINGDO NOT PRINT DO NOT PRINT DO NOT PRINT DO NOT PRINTC lass VI and VII$$$Class IV$$$Class V$$$Form8594(Rev. 2-2006)$Part IIIU serid: _____Leading adjust: 0% Draft Ok to PrintPAGER/ (17-Feb-2006)(Init. & date)Filename: D:\USERS\vghcb\documents\Epicfiles\2005 files\ 1 of 3 Instructions for Form 859410:30 - 17-FEB-2006 The type and rule above prints on all proofs including departmental reproduction proofs.

6 MUST be removed before of the TreasuryInternal Revenue ServiceInstructions for Form 8594 (Rev. February 2006) Asset Acquisition Statement Under Section 1060 Section references are to the Internal Revenue Code unless otherwise (d) for special reportingof the assets (other than goodwill orGeneral Instructionsrequirements. However, the purchasegoing concern value) as shown in theof a partnership interest that ispurchaser s financial accountingPurpose of Formtreated for federal income taxbooks and records; orBoth the seller and purchaser of apurposes as a purchase of A license, a lease agreement, agroup of assets that makes up a tradepartnership assets, which constitute acovenant not to compete, aor business must use Form 8594 totrade or business, is subject tomanagement contract, anreport such a sale if goodwill or goingsection 1060.

7 In this case, theemployment contract, or other similarconcern value attaches, or couldpurchaser must file Form 8594 . Seeagreements between purchaser andattach, to such assets and if theRev. Rul. 99-6, which is on page 6 ofseller (or managers, directors,purchaser s basis in the assets isInternal Revenue Bulletin 1999-6 atowners, or employees of the seller).determined only by the amount purchaser sfor the , and Regulations sectionconsideration is the cost of (b)(4).Form 8594 must also be filed if theassets. The purchaser spurchaser or seller is amending anconsideration is the amount To Fileoriginal or a previously filedFair market market valueGenerally, attach Form 8594 to yoursupplemental Form 8594 because ofis the gross fair market valueincome tax return for the year inan increase or decrease in theunreduced by mortgages, liens,which the sale date s cost of the assets or thepledges, or other liabilities.

8 However,amount realized by the the amount allocated to anyfor determining the seller s gain orasset is increased or decreased afterloss, generally, the fair market valueWho Must Filethe year in which the sale occurs, theof any property is not less than anyGenerally, both the purchaser andseller and/or purchaser (whoever isnonrecourse debt to which theseller must file Form 8594 and attachaffected) must complete Parts I andproperty is to their income tax returns (FormsIII of Form 8594 and attach the formClasses of following1040, 1041, 1065, 1120, 1120S, etc.)to the income tax return for the yeardefinitions are the classifications forwhen there is a transfer of a group ofin which the increase or decrease isdeemed or actual Asset that make up a trade ortaken into (defined below) and theClass I assets are cash andPenaltiespurchaser s basis in such assets isgeneral deposit accounts (includingdetermined wholly by the amountsavings and checking accounts) otherIf you do not file a correct Form 8594paid for the assets.

9 This appliesthan certificates of deposit held inby the due date of your return andwhether the group of assetsbanks, savings and loan associations,you cannot show reasonable cause,constitutes a trade or business in theand other depository may be subject to penalties. Seehands of the seller, the purchaser, orsections 6721 through II assets are actively property within the meaningDefinitionsIf the purchaser or seller is aof section 1092(d)(1) and RegulationsTrade or group ofcontrolled foreign corporation (CFC),section (d)-1 (determinedassets makes up a trade or businesseach shareholder should attachwithout regard to section 1092(d)(3)).

10 If goodwill or going concern valueForm 8594 to its Form addition, Class II assets includecould under any circumstances attachcertificates of deposit and are not required toto such assets. A group of assets cancurrency even if they are not activelyfile Form 8594 if any of the followingalso qualify as a trade or business if ittraded personal property. Class as an active trade orassets do not include stock of target A group of assets that makes up abusiness under section 355 (relatingaffiliates, whether or not activelytrade or business is exchanged forto distributions of stock in controlledtraded, other than actively tradedlike-kind property in a transaction tocorporations).