Transcription of Cash Flow Analysis Borrower Name:

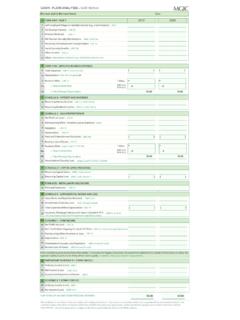

1 Fannie Mae Form 1084 Page Flow AnalysisBorrower name : _____A lender may use this worksheet to prepare a written evaluation of its Analysis of a self-employed Borrower s personal income, including the business income or loss, reported on the Borrower s personal income tax returns. The purpose of this written Analysis is to determine the amount of stable and continuous income that will be available to the borrowerfor loan qualifying Form 1040 Individual Income Tax Income , Salaries, Tipsconsidered elsewhere(-)_____(-) Interest Income (+)_____(+) and Local Tax Refunds(-)_____(-) Alimony Received(-)_____(-) Schedule D (Income) Loss(+/-)_____(+/-)_____ Other (Gains) Loss (+/-)_____(+/-)_____ Distributions(+)_____(+) Annuities(+)_____(+) E (Income) Loss(+/-)_____(+/-) Unemployment Compensation(-)_____(-) Security Benefits(+)_____(+) Other (Income) Loss(+/-)_____(+/-) _____(+/-)_____(+/-)_____IRS Form 2106 Employee Business Unreimbursed Expenses(-)_____(-) (+)_____(+)_____Schedule B (IRS Form 1040) Interest and Ordinary Dividends17.

2 Nonrecurring Interest Income(-) _____(-) _____18. Nonrecurring Dividend Income(-) _____(-) _____ScheduleC (IRS Form 1040) Profit or Loss from Business: Sole Proprietorship19. Nonrecurring Other (Income) Loss/Expenses(+/-) _____(+/-) _____20. Depletion(+) _____(+) _____21. Depreciation(+) _____(+) _____22. Travel, Meals, and Entertainment (-) _____(-) _____23. Business Use of Home (+) _____(+) _____24. Amortization/Casualty Loss(+) _____(+) _____Schedule D(IRS Form 1040) Capital Gains and Losses25. Recurring Capital Gains (+)_____(+)_____IRS Form 4797 Sales of BusinessProperty26. Recurring Capital Gains(+)_____(+)_____IRS Form 6252 Installment Sale Income 27. Principal Payments Received(+)_____(+)_____Fannie Mae Form 1084 Page 2 Schedule E (IRS Form 1040) Supplemental Income and Loss Note: A lender may use Fannie Mae Rental Income Worksheets (Form 1037 or Form 1038) to calculate individual rental income (loss) reported on Schedule E.

3 Year_____ Year_____ 28 . Royalties Received (+)_____ (+)_____ 29 . Total Expenses (- )_____ (-)_____ 30. Depletion (+)_____ (+)_____ Schedule F (IRS Form 1040) Profit or Loss from Farming 31 . Non-Tax Portion Ongoing Cooperative Distribution and Commodity Credit Corporation Payments (+)_____ (+)_____ 32 . Nonrecurring Other (Income) Loss (+/-)_____ (+/-)_____ 33 . Depreciation (+)_____ (+)_____ 34 . Amortization/Casualty Loss/Depletion (+)_____ (+)_____ 35 . Business Use of Home (+)_____ (+)_____ _____ Schedule K-1 Ownership in the business <25% -- Borrower does not meet definition of self-employed Business income reported on Schedule K-1 may be used to qualify only when the Borrower has a documented stable history of receiving cash distributions of income from the business consistent with the level of business income being used to qualify. Partnership Schedule K-1 (IRS Form 1065) 36.

4 Ordinary Income, Net Rental Real Estate Income, Other Net Rental Income _____ _____ 37. Distributions _____ _____ 38. Lesser of line 36 or line 37 (+)_____ (+)_____ 39 . Guaranteed Payments to Partner (+)_____ (+)_____ S Corporation Schedule K-1 (IRS Form 1120S) 40. Ordinary Income, Net Rental Real Estate Income, Other Net Rental Income _____ _____ 41. Distributions _____ _____ 42. Lesser of line 40 or 41 (+)_____ (+)_____ Personal Income Total _____ _____ Fannie Mae Form 1084 Page 3 Schedule K-1 -- Ownership in the business 25% or greater Borrower meets definition of self-employed Business income reported on Schedule K-1 may be used to qualify the Borrower only when the Borrower has a documented stable history of receiving cash distributions of income from the business consistent with the level of business income being used to qualify.

5 Partnerships and S Corporations The Borrower s proportionate share of adjustments to business cash flow may be used to qualify only when: the Borrower can document ownership and access to income, and has a documented stable history of receiving cash distributions of income from the business consistent with the level of business income being used to qualify; the business has adequate liquidity to support withdrawal of earnings; and the business has positive sales and earnings trends. Year_____ Year_____ Partnership Schedule K-1 (IRS Form 1065) 43 . Ordinary Income (Loss), Net Rental Real Estate Income (Loss), Other Net Rental Income (Loss) (+/-)_____ (+/-)_____ 44 . Proportionate Share of Adjustments to Business Cash Flow Income (Loss) Form 1065; enter result from line 59 below (+/-)_____ (+/-)_____ 45 . Subtotal _____ _____ 46 . Distributions _____ _____ 47. Lesser of line 45 or line 46 (+)_____ (+)_____ 48.

6 Guaranteed Payments to Partner (+)_____ (+)_____ 49. Partnership Total (line 47 + line 48 ) _____ _____ IRS Form 1065 - Adjustments to Business Cash Flow 50. Pass-through (Income) Loss from Other Partnerships (+/-)_____ (+/-)_____ 51 . Nonrecurring Other (Income) Loss (+/-)_____ (+/-)_____ 52 . Depreciation (+)_____ (+)_____ 53 . Depletion (+)_____ (+)_____ 54 . Amortization/Casualty Loss (+)_____ (+)_____ 55 . Mortgages or Notes Payable in Less than 1 Year (- )_____ (-)_____ 56 . Travel, Meals, and Entertainment (- )_____ (-)_____ 57 . Subtotal _____ _____ 58 . Multiply by Borrower % of Ownership (x)_____ (x)_____ 59. Proportionate Share of Adjustments to Business Cash Flow _____ _____ S Corporation Schedule K-1 (IRS Form 1120S) 60. Ordinary Income (Loss), Net Rental Real Estate Income (Loss), Other Net Rental Income (Loss) (+/-)_____ (+/-)_____ 61.

7 Proportionate Share of Adjustments to Business Cash Flow Income (Loss) Form 1120S; enter result from line 74 below (+/-)_____ (+/-)_____ 62 . Subtotal _____ _____ 63 . Distributions _____ _____ 64. Lesser of line 62 or line 63 (+)_____ (+)_____ 65. S Corporation Total _____ _____ IRS Form 1120S - Adjustments to Business Cash Flow 66 . Nonrecurring Other (Income) Loss (+/-)_____ (+/-)_____ 67 . Depreciation (+)_____ (+)_____ 68 . Depletion (+)_____ (+)_____ 69. Amortization/Casualty Loss (+)_____ (+)_____ 70 . Mortgages or Notes Payable in Less than 1 Year (- )_____ (-)_____ 71 . Travel, Meals, and Entertainment (- )_____ (-)_____ 72 . Subtotal _____ _____ 73 . Multiply by Borrower % of ownership (x)_____ (x)_____ 74. Proportionate Share of Adjustments to Business Cash Flow _____ _____ Fannie Mae Form 1084 Page 4 Regular Corporation IRS Form 1120 Income derived from the following Analysis may be used to qualify when: the Borrower is 100% owner of the business, the business has adequate liquidity to support withdrawal of earnings, and the sales and earnings trends of the business are positive.

8 75. Taxable Income _____ _____ 76. Total Tax (- )_____ (-)_____ 77. Nonrecurring (Gains) Losses (+/-)_____ (+/-)_____ 78. Nonrecurring Other (Income) Loss (+/-)_____ (+/-)_____ 79. Depreciation (+)_____ (+)_____ 80. Depletion (+)_____ (+)_____ 81. Amortization/Casualty Loss (+)_____ (+)_____ 82. Net Operating Loss and Special Deductions (+)_____ (+)_____ 83. Mortgages or Notes Payable in Less than 1 Year (- )_____ (-)_____ 84. Travel, Meals, and Entertainment (- )_____ (-)_____ 85 . Dividends Paid to Borrower (- )_____ (-)_____ 86 . Corporation Total _____ _____ Totals Personal Income Total _____ _____ Partnership Total [line 49] _____ _____ S Corporation Total [line 65] _____ _____ Corporation Total [line 86] _____ _____ (Include only when the Borrower owns 100% of the business) Grand Total _____ _____ _____ The lender may use a profit and loss statement audited or unaudited for a self-employed Borrower s business to support its determination of the stability or continuance of the Borrower s income.

9 Allowable add-backs include depreciation, depletion, and other non-cash expenses as identified above. Year-to-Date Profit and Loss Statement Salary/Draw to Individual _____ Net Profit _____ x_____% o wnership = _____ Total Allowable Add-backs _____ x _____% o wnership = _____ Year-to-Date Total _____ Instructions Page 1 CASH FLOW Analysis (Fannie Mae Form 1084) Instructions IRS Form 1040 Individual Income Tax Return Line 1 - Total Income: Begin with Total Income, which represents the Borrower 's gross income before adjustments. Line 2 Wages, Salaries, and Tips considered elsewhere: Subtract any income reported on Form 1040 that has been verified and underwritten based on current information or that does not belong to the Borrower . This type of income includes salary and hourly compensation, income from a spouse or ex-spouse that will not be used for underwriting purposes, or other income more appropriately underwritten based on current earnings rather than historical.

10 Cross-reference the amount reported on Form 1040 against the amount indicated on the Borrower 's Form W-2. Line 3 Tax-exempt Interest Income: Add any tax-exempt interest income included on Form 1040 to the Total Income if it is likely to continue and is verified as recurring income. Taxable interest income and dividend income reported on Form 1040 will be addressed by analyzing Schedule B (Form 1040). (See Schedule B (IRS Form 1040) Interest and Ordinary Dividends below.) Line 4 State and Local Tax Refunds: Subtract from Total Income all taxable refunds, credits, or offsets of state and local income taxes reported on Form 1040. A tax refund cannot be included as qualifying income since it has been accounted for in the previous year's gross income. Line 5 Nonrecurring Alimony Received: Subtract from Total Income any alimony income that does not meet all of the following criteria: the receipt of alimony income has been documented as stable for at least 6 months, the payments will be ongoing and consistent with the level reported on Form 1040 for a minimum of three years, and the alimony payments are made as a result of a divorce decree or written and signed agreement that is a legal obligation.