Transcription of Mastering the Cash Flow Statement & Free Cash Flow CFA ...

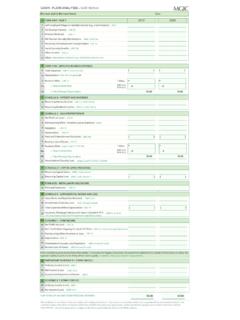

1 1 CFA LEVEL I 2013 2012 Kaplan Financial Limited1 Financial Reporting and AnalysisMastering the cash flow Statement & free Cash FlowCFA Levels I & of cash flow StatementNet income from accrual accounting does not tell us about the sources and uses of cashto meet liabilities and operating needsThe Statement of cash flows has three components under both IFRS and US GAAP: Cash provided or used by operatingactivities Cash provided or used by investingactivities Cash provided or used in financingactivitiesLOS Compare/Classify: CFAI pg 253 Schweser pg 109 Understanding the cash flow Statement2 CFA LEVEL I 2013 2012 Kaplan Financial GAAP vs.

2 IFRSI nterest receivedInterest paidDividends receivedDividends paidTaxes paidBank overdraftCFOCFOCFOCFFCFOCFFCFO or CFICFO or CFFCFO or CFICFO or CFFCFO or CFI & CFF* GAAP(SFAS 95)IAS GAAP(IAS 7)* Considered part of cash and cash equivalentsLOS Contrast: CFAI pg 255 Schweser pg 111 Understanding the cash flow StatementStatement of cash flow : Direct vs. Indirect MethodDirect vs. indirect method refers only to the calculation of CFO, the value of CFO is the same for both methods; CFI and CFF are unaffected Direct method: Identify actual cash inflows and outflows; , collections from customers, amount paid to suppliers Indirect method: Begin with net income and make necessary adjustments to get operating cash flowLOS Distinguish/Describe: CFAI pg 256 Schweser pg 112 Understanding the cash flow Statement3 CFA LEVEL I 2013 2012 Kaplan Financial Limited3 Linkages Between StatementsAccounts Receivable T AccountAmount B/FwdSalesAmount C/Fwd18,00020,000200,000218,000218,000 Cash collections198,000 This year s balance sheetLast year s balance sheetThis year s income statementLOS Describe.

3 CFAI pg 266 Schweser pg 114- 5 Understanding the cash flow StatementCash Inflows and OutflowsGeneral rules regarding increases and decreases in balance sheet items over time:IncreaseDecreaseAssetsoutflowinflow Liabilities & Equity : An increase in AR or inventory uses cashAn increase in payables generates cashAdjust net income for these changes (indirect)Understanding cash flow StatementsLOS Describe: CFAI pg 267 Schweser pg 1154 CFA LEVEL I 2013 2012 Kaplan Financial Limited4 Ecclestone Industries ExampleEcclestone Industries has the following income Statement for 20X9 and balance sheets for 20X8 and 20X9. You are to construct the Statement of cash flows using the indirect information:Equipment was purchased for $50,000 Ecclestone has a tax rate of 40%LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow StatementIncome Statement for Year to 31 December 20X9 Sales revenueExpenses:Cost of goods soldSalariesDepreciationInterestGain from sale of PPEPre-tax incomeProvision for taxesNet income$ 200,000105,00095,00020,000115,00040,0007 5,000$ 80,00010,00014,0001,000 LOS Describe.

4 CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement5 CFA LEVEL I 2013 2012 Kaplan Financial Limited5 Ecclestone Balance Sheet DataBalance SheetsCurrent assetsCashAccounts receivableInventoryNon-current assetsGross PPEA ccum. Assets20X8$ 18,00018,00014,000282,000252,00020X9$ 66,00020,00010,000312,000324,000(80,000) (84,000)LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow StatementBalance SheetsCurrent liabilitiesAccounts payableSalaries payableInterest payableTaxes payableDividends payableNoncurrent liabilitiesBondsDeferred taxesStockholders equityCommon stockRetained earningsTotal Liabilities & Equity20X8$ 10,00016,0006,0008,0002,00020,00030,0001 00,00060,000252,00020X9$ 18,0009,0007,00010,00012,00030,00040,000 80,000118,000324,000 LOS Describe.

5 CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement6 CFA LEVEL I 2013 2012 Kaplan Financial Limited6 Direct Method CFO1. Take each income Statement item in turn , sales2. Move to the balance sheet and identify asset and liability accounts that relate to that income Statement item , accounts receivable3. Calculate the change in the balance sheet item during the period (ending balance opening balance)4. Apply the rule:Increases in an asset: deduct Increase in a liability: addDecrease in an asset: addDecrease in a liability: deductLOS Convert: CFAI pg 302 Schweser pg 120 Understanding the cash flow StatementDirect Method the income Statement amount by the change in the balance off the items dealt with in both the income Statement and balance to the next item on the income Statement and depreciation/amortization and gains/losses on the disposal of assets as these are non-cash or non-CFO itemsLOS Convert.

6 CFAI pg 302 Schweser pg 120 Understanding the cash flow Statement7 CFA LEVEL I 2013 2012 Kaplan Financial moving down the income Statement until all items included in net income have been addressed applying steps up the amounts and you have CFOD irect Method CFOLOS Convert: CFAI pg 302 Schweser pg 120 Understanding the cash flow StatementCash InflowsSalesLess: Increase in A/RCash collected from customersDirect cash outflowsCost of goods soldAdd: Decrease in inventoryPurchasesAdd: Increase in A/PCash paid to suppliersOperating expense (wages)Less: Decrease in salaries payableCash paid to employees200,000(2,000)(80,000)4,000(76, 000)8,000198,000(68,000)(10,000)(7,000)( 17,000)Direct Method CFO-8 LOS Convert: CFAI pg 302 Schweser pg 120 Understanding the cash flow Statement8 CFA LEVEL I 2013 2012 Kaplan Financial Limited8(28,000)(40,000)10,0002,000(1,00 0)1,000 Direct Method, outflowsInterest ExpenseAdd: Increase in interest payableCash interest paidTax ExpenseAdd: Increase in deferred tax payableAdd: Increase in taxes payableCash taxes paid $$CFO085,000(30,000)-7 LOS Convert.

7 CFAI pg 302 Schweser pg 120 Understanding the cash flow StatementIndirect Method CFOCFO = NI + NCC - WCinvLOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement + Depreciation+ Amortisation+ Loss on asset disposal- Gain on asset disposal+ Loss on early debt retirement- Gain on early debt retirement+ Increase in DTL, decrease in DTA- Decrease in DTL, increase in DTA+ Non cash expenses (provisions) Current assets excluding cash and investments Current liabilitiesexcluding debt instruments and dividends payable= change in non-cash working capital9 CFA LEVEL I 2013 2012 Kaplan Financial Limited9 Indirect Method CFO (Alternative)LOS Describe.

8 CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement75,000 + 4,000 + 6,000 = 85,000+ Depn- Disposal gain + DTLNCCC urrent assets-Cash & Inv Current liabilities-Debt & divs Working Capital$14,000(20,000)10,0004,00020x820x 9$$50,000 96,000(18,000) (66,000)32,000 30,00042,000 56,000(2,000) (12,000)40,000 44,000(8,000) (14,000) WC = (6,000)CFO = NI + NCC - WCinv-6 Calculating CFICFI = investment in assets cash received on asset salesNet book value = Gross PPE accumulated depreciationGain (loss) on sale = sales price net book valueLOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement10 CFA LEVEL I 2013 2012 Kaplan Financial Limited10 Ecclestone CFI Gross Plant and PPEA dditions PPE disposal Ending PPE282,00050,000(20,000)312,000 Accumulated Acc.

9 ExpenseAD for disposalEnd Acc. ,00014,000(10,000)84,000 Calculating NBV of asset soldNBV of disposal = 20,000 10,000 = 10,000-5 LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow StatementCFI = cash additions cash received on disposalSale ProceedsNBV of disposal Gain(loss) on sale 30,00010,00020,000$CFI = additions + proceedsCFI = $50,000 + $30,000 = $20,000 Ecclestone CFI-2 LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement11 CFA LEVEL I 2013 2012 Kaplan Financial Limited11 Computing CFF Change in debt Change in common stock Cash dividends paidNet incomeDividends declared in retained earnings$X(X)XDividends declared Dividends payableCash paid$(X)X(X)LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement Change in debt Change in common stock Cash dividends paidNet incomeDiv declared in R/E$75,000(17,000)58,000 Dividends decl.

10 Div. payableCash div. paid$(17,000)10,000(7,000)Ecclestone CFF$10,000(20,000)(7,000)(17,000)-7 LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow Statement12 CFA LEVEL I 2013 2012 Kaplan Financial Limited12$85,000(20,000)(17,000)48,00018 ,00066,000 Putting the cash flow Statement TogetherCash flow from operationsCash flow from investmentsCash flow from financingNet increase in cashCash balance 12/31/X8 Cash balance 12/31/X9-6 LOS Describe: CFAI pg 267 Schweser pg 115 Understanding the cash flow StatementFree cash flow (FCF) FCF is cash available for discretionary uses Frequently used to value firms FCFF = NI + NCC - WCInv + Int (1-T) FCInv FCFF = CFO + Int (1-T) FCInv FCFE = CFO FCInv + Net debt increaseLOS Calculate/Interpret.