Transcription of Notes on SAMPLE Form 3115 - myCPE

1 Notes on SAMPLE form 3115 1. General a. The SAMPLE form 3115 relates to a residential rental property (where the entire building depreciated using recovery period, and no allocation was previously made to land improvements or personal property). b. It assumes that the reduced reporting rules for "qualified small taxpayers" apply. i. This should be true for most of clients. 1. A "qualified small taxpayer" is a taxpayer whose average annual gross receipts, as determined under (a)-3(h}(3}, for the three preceding taxable years is less than or equal to $10,000,000. a. If the taxpayer doesn't meet this requirement, see form 3115 for complete filing instructions in Rev.))

2 Proc. 2019-43, Sec. 6 .. c. This SAMPLE form 3115 relates to used property acquired before Sept. 28, 2017 and therefore does not claim bonus depreciation. Don't include bonus depreciation for the acquisition of used property unless acquired and placed in service after Sept. 27, 2017. d. I recommend that you attach form 2848 in case the IRS has any questions. i. This form 3115 assumes that you'll attach a power of attorney to it (since the contact person on page one is a CPA representative). e. Use this accounting method change if you've used the accounting method on more than one preceding tax return. f.

3 You don't receive an acknowledgement of filing from the IRS. But they'll contact you if they have any questions. 2. These method changes can be prepared during the "offseason." a. You can prepare a method change for the 2019 tax year in November or December of 2019. i. The 481(a) calculations are based upon ending depreciation shown on the client's 2018 tax return. 3. Documents in effect a. At the time of preparing this SAMPLE form 3115, the following documents were operative: i. Rev. Proc. 2015-13 describing accounting method changes generally. ii. Rev. Proc. 2019-43 covering automatic changes. 1. The accounting method change on the SAMPLE form is an "automatic" change; that means that there is no filing fee, and you can file form 3115 after the end of the year.

4 1 iii. Rev. Proc. 2016-1 covering other matters related to filing automatic accounting changes (this has been superseded however Rev. Proc. 2019-43 continues to refer to it). iv. form 3115 last updated 12-2018 (instructions revised as of Jan. 18, 2019). 4. Sec. 481(a) adjustment. a. Deduct in the year of change. i. This SAMPLE relates to the 2019 form 1065, so the negative Sec. 481 adjustment would be deducted on the 2019 tax return. ii. The adjustment (deduction) is based upon the difference in accumulated at the end of the prior year. 1. So, for example, if you've taken $12,000 in cumulative depreciation at 12/31/18 on a rental property, but you should have taken cumulative depreciation $28,000 as of 12/31/18, you'd take an additional deduction of $16,000 on your 2016 tax return.

5 2. For the 2019 tax year (assumed in this example to the be year's tax return to which you attach form 3115), you'd compute depreciation using the new method b. You also need to make corresponding changes to the client's accumulated depreciation. c. See form 3115 instructions for more information. 5. Filing instructions (two Forms 3115 must be filed) a. form 3115 must be filed by the due date of the return, including extensions. i. There's a special waiver if you didn't extend the return --can file within the 6-month period following original due date. See Rev. Proc. 2015-13. b. Client and you both sign form 3115.

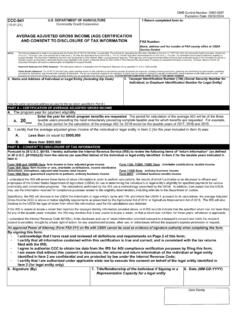

6 C. Attach copy to tax return that you file with the IRS (but file copy with Ogden first -see below). d. Also, mail signed copy (no later than the time you file the tax return) to: Internal Revenue Service Ogden, UT 84201 M/5 6111 2 form 3115 Application for Change in Accounting Method (Rev. December 2018) Department of the Treasury Internal Revenue Service Goto for instructions and the latest information. Name of filer (name of parent corporation if a consolidated group) (see instructions) Identification number (see instructions) 99-9999999 Principal business activity code number (see instructions) 203 Real Estate Investors, LLC 53110 0MB No.

7 1545-2070 Number, street, and room or suite no. If a box, see the instructions. Tax year of change begins (MM/DD/YYYY) 1 / O 1 / 2 0 19 203 N Street NE Tax year of change ends (MM/DD/YYYY) 12 / 31 / 2 0 19 City or town, state, and ZIP code Name of contact person (see instructions) Auburn, WA 98002 Greaorv L White Name of applicant(s) (if different than filer) and identification number(s) (see instructions) I Contact person's telephone number If the annlicant is a member of a consolidated arouo. check this box .. If form 2848, Power of Attorney and Declaration of Representative, is attached (see instructions for when form 2848 is required), check this box.

8 X Check the box to indicate the type of applicant. Cooperative (Section 1381) Check the appropriate box to indicate the type of accounting method change being requested. See instructions. X Partnership Corporation S corporation [R] Depreciation or Amortization ~ Individual Controlled foreign corporation (Section 957) 10/50 corporation (Section 904(d)(2)(E)) Qualified personal service corporation (Section 448(d)(2)) Insurance company (Section 816(a)) Insurance company (Section 831) Other (specify) D Financial Products and/or Financial Activities of Financial Institutions D Other (specify).. _____ _ Exempt organization.

9 Enter Code section Caution: To be eligible for approval of the requested change in method of accounting, the taxQayer must provide all information that is relevant to the taxgayer or 1o the taxpayer's requested change in method of accounting. This includes (1) all relevant information reguested on this form 3115 (including its instructions) and (2) any olher relevant even if not specifically requested on form 3115. The taxpayer must attach all applicaole statements requested throughout tnis form . n ormat1on or utomat1c ange equest 1 Enter the applicable designated automatic accounting method change n Enter only one DCN, except as provided for in guidance publish~b 'Other,' and provide both a description of the change an~ h N') for the requested automatic change.

10 E requested change has no DCN, check guidance providing the automatic change. See instructions. ~ a (1) DCN: 7 (2) DCN: ____ (3) DCN: ____ (4) DCN: ___ (5) DCN: ____ (6) DCN: ___ _ (7) DCN: --, (8) DCN: ____ (9) DCN: ____ (10) DCN: ___ (11) DCN: (12) DCN: ___ _ b Other O Description 2 Do any of the eligibility rules restrict the applicant from filing the requested change using the automatic change procedures (see instructions)? If 'Yes,' attach an explanation .. 3 Has the filer provided all the information and statements required (a) on this form and (b) by the List of Automatic Changes under which the applicant is requesting a change?