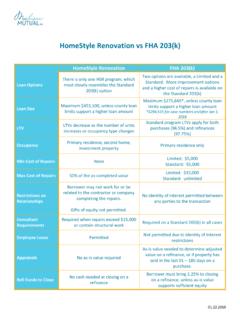

Transcription of Official Underwriting Sample Package

1 Property: Sample Retail Owner Occupied Requested loan Amount: $750,000 Property Located At: 100 Main Street Los Angeles, California 90012 Submitted By: John Smith Your Company 100 Main Street Any City, California 90001 Email: Official Underwriting Sample Package Up to 2 Photos of the retail building on the cover pagePhone: (713) 568-1837 Executive Summary Property Type Requested loan Amount loan Purpose loan Term (Years) Amortization(Years) Requested Interest Rate loan To value Debt Service Coverage Ratio Present Occupancy % Existing loan Balance Underwriting Reserves Min. Vacancy Reserve Min. Management Fee Summary Retail $750,000 Refinance 5 25 100 $ 635,000 Sample Retail Owner Occupied The purpose of the loan is to refinance this single-story retail building.

2 The property is owner-occupied by ABC Rentals. This Underwriting analysis is based on the property being rented at market rent, with no income or expenses attributable to the business. ABC Rentals has been in business since 1996; the net profit in 2002 was $123,000. The borrower owns several investment properties in the area. The borrower is looking to refinance the existing mortgage and use the remaining proceeds to purchase new equipment and remodel parts of the building. Generally, Underwriting owner-occupied commercial real estate consists of two primary elements: (1) real estate value and (2) business value . For example, when analyzing an owner-occupied property, a lender may analyze the value of the real estate based on its ability to generate income under a market rent scenario.

3 This procedure provides insight to the projected value of the real estate, and its ability to generate rental income, should it be leased to a tenant other than the owner-occupant; as what could be the case in the event of a foreclosure or if the owner-occupant business closes. Once a determination of the real estate value is made, a lender may then analyze the owner-occupant's business to ascertain whether the business generates sufficient income to service the proposed debt. Therefore, the lender is assured that the debt service can be covered under both scenarios. Testing value : The primary real estate Underwriting test for owner-occupied properties includes an analysis of the property's ability to generate income under a "market rent" scenario-as if the owner-occupant was not the tenant and the Page 2 of 13 Replacement Reserve TILC Reserve $ 0.

4 60/SF Here is where we create a summary of you project and add any importantinformation that needs to be clarified or is not obvious. Sample Retail Owner Occupied space was leased to a non-owner tenant. To complete this analysis, the following must be known: 1. Estimated Market Rent for the owner-occupied space(s). 2. Typical lease structure for the owner-occupied space(s). a. Average lease term (that is customary for the respective market). b. Items paid by lessee (tenant) vs. lessor (landlord). Entering loan data into LoanSizer: Complete the loan , Property and Building tabs as applicable. On the Rent Roll tab, enter the owner-occupant as a tenant. Case 1 - Owner has a lease: In many cases, the owning-entity (the entity that owns the real estate) has a lease with the tenant-entity (the owning-entity's business); this is known as a synthetic lease and is commonly done for tax or accounting purposes.

5 While this lease may be written at market rent, it is not an arm's-length transaction, and the rental income must be "marked-to-market." This is done by examining the market for comparable leases (similar properties that are leased to non-owning tenants), and entering the market rent in the Contract Rent fields. Case 2 - Owner has no lease: In instances where the owning-entity has no lease with the tenant-entity, you must enter the owner-occupant as a tenant using market rent and a market lease structure. For example, if similar properties are leased at $ per square foot per year, with a 3-year lease term, and real estate taxes, insurance and utilities are included, then you should enter the owner-occupant as a tenant under these lease conditions. This demonstrates a projection of how the property would perform if it was leased to a non-owner tenant.

6 The following describes the steps required to enter an owner-occupant tenant. Rent Roll tab: Tenant Name: Enter the name of the owner-occupant business. Contract Rent: Enter the estimated market rent [Note: make certain to apply the appropriate income modifier ( , $/Yr, $/SF/Yr, etc.)]. Leased Area: Enter the leased area in square feet. Contract Rent/SF: This field calculates automatically. Lease Start: Enter today's date. Lease Expire: Enter the projected lease expiration date. For example, if it is common for comparable space to be rented on a 3-year lease term, enter today's date plus 3 years. Occupied Since: Enter the year the owner-occupant took physical occupancy. Tenant Type: Enter the general use type. Est. Market Rent: Enter the estimated market rent. By default, LoanSizer auto-populates this field with the Contract Rent entered for the tenant.

7 Suite: Enter the Suite Number, if applicable. Lease Options: Enter the typical number of lease options; if unknown, leave blank. Option Terms (yrs): Enter the typical option terms in years; if unknown, leave blank. Borrower Affiliated: Enter a check in this field to show the space is owner-occupied. Credit Rated: Enter a check in this field if the owner-occupant is credit rated ( , Standard & Poor's BBB- or above). Income / Expense tab: When entering income and expenses for an owner-occupied property, enter only the income and expenses that are attributable to the real estate, not the operating business. The goal is to develop a snapshot of the net income the property would produce if it was leased under a market rent scenario. Items related to the operating business ( , gross sales receipts, payroll, health insurance, employee benefits, etc.)

8 Should not be include in the real estate analysis. Common "Income" items: - Base rent - Expense reimbursements (if comparable leases indicate that certain expenses are reimbursed) Common "Expense" items: - Real estate taxes - Property insurance Page 3 of 13 Sample Retail Owner Occupied - Utilities - Repairs and Maintenance - Management fees - Advertising and marketing - General and administrative Underwriter Info tab: loan Term: Enter the desired term in years. Interest Rate Index: Select the appropriate index ( , Prime Rate, 10 Yr US Treasury, etc.). If unknown, select "To Be Determined". Current Index Yield: Enter the current yield of the selected index ( , if the present yield of Prime Rate is , enter ). Interest Rate Spread: Enter the requested interest rate spread (this is similar to a "margin"); the sum of the Current Index Yield plus the Interest Rate Spread will equal your requested interest rate.

9 Other fields: Unless you have a specific reason to change the remaining fields, use the Suggested values. loan Results: You loan results will be displayed in the Originator loan Results window on the top right of the screen. These loan results display the calculations based on an analysis of the property under a market rent scenario which demonstrates the projected ability of the property to generate rental income. For owner-occupied properties, lenders will often want to review the financials of the owner's business to gauge its financial strength and ability to service the proposed loan . As the business analysis is not real estate-related, this analysis can not be completed in LoanSizer. When submitting an owner-occupied property to a lender, it is helpful to include a description of the owner-occupant's business.

10 Your description should include the following information: - Type of business - Years in operation - Profit and Loss statements (for 3 years) - Balance Sheet - Summary of Borrower's experience Page 4 of 13 Underwriting Analysis loan Information Underwriting Results Property Type loan Purpose loan Term 5 yrs loan Amortization Requested Interest Rate Interest Rate Index Current Index Yield Interest Rate Spread Last Appraised value Underwriting Constraints Notes: loan Type Existing loan Balance Max. LTV Min. DSCR Min. Vacancy Reserve Min. Management Fee Interest Accrual Method Interest Rate Rounding TI/LC Stress DSCR Rent Roll Start Date Avg. Lease Term (months) Expense Growth Rate Retail Refinance 25 yrs Fixed To Be Determined $635,000 $0 Actual 360 No Rounding 11/13/2005 36 Replacement Reserve $ $ TILC Reserve Sample Retail Owner Occupied Max.

![Section 2.01c: Texas Cash-Out [50(a)(6)] Refinance First ...](/cache/preview/b/3/1/a/6/9/1/d/thumb-b31a691d22b1f85eee437442f2f97177.jpg)