Transcription of Rating Methodology - riskcalc.moodysrms.com

1 RiskCalcTMFor Private Companies: Moody's Default ModelMay 2000 ContactPhoneNew YorkEric BoralLea V. CartyRISKCALCTM FORPRIVATECOMPANIES: MOODY'SDEFAULTMODELR ating MethodologyRating Methodologycontinued on page 3 Rating MethodologySummaryThis report describes and documents Moody's version of its RiskCalcTM default model for pri-vate firms. RiskCalcTManalyzes financial statement data to produce default probability predic-tions for corporate obligors - particularly those in the middle market. We discuss the model'sderivation in detail, analyze its accuracy, and provide context for its application. The model'skey advantage derives from Moody's unique and proprietary middle market private firm finan-cial statement and default database (Credit Research Database), which comprises 28,104 com-panies and 1,604 defaults.

2 Our main insights and conclusions are: The relationship between financial variables and default risk varies substantially betweenpublic and private firms. An important consequence of this is that default models based onpublic firm data and applied to private firms will likely misrepresent actual default risk. RiskCalcTMgenerates 1- and 5-year expected default frequencies, as well as a mapping intoMoody's standard Rating categories. Hence, the meaning of the model output is easily under-stood and amenable to benchmarking and quantitative portfolio risk management techniques. Comprehensive testing and validation suggest that RiskCalc's predictive power is superiorto that of other publicly available benchmark models and is robust across non-financialindustry sectors, and over time.

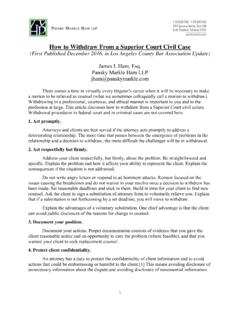

3 RiskCalcTMwas developed to achieve maximum predictive power with the smallest number ofinputs. It requires just 10 financial ratios & indicators computed from 17 basic financial inputs. RiskCalc's predictive power derives, in part, from its meticulous transformation of inputfinancial ratios, which are highly 'nonnormally' distributed, as well as the large number ofdefaulting private firms used in its estimation. Moody's Default Model For Private Companies: An Anecdotal Example of Chai-Na-Ta Corp Defaulted January 28, 200019931994199519961997199819990246810 Exhibit company, headquartered in British C olumbia, is the world's largest producer ofNorth American ginseng. The company farms, processes and distributes the under continued pressure from depressed ginseng prices, the firm previous eight quarters of data were used f or each RiskCalc s Rating Methodology Copyright 2000 by Moody s Investors Service, Inc.

4 , 99 Church Street, New York, New York 10007. All rights reserved. ALL INFORMATION CONTAINED HEREIN ISCOPYRIGHTED IN THE NAME OF MOODY S INVESTORS SERVICE, INC. ( MOODY S ), AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISEREPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FORANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY S PRIORWRITTEN information contained herein is obtained by MOODY Sfrom sources believed by it to be accurate and reliable. Because of the possibility ofhuman or mechanical error as well as other factors, however, such information is provided as is without warranty of any kind and MOODY S, in particular, makes norepresentation or warranty, express or implied, as to the accuracy, timeliness, completeness, merchantability or fitness for any particular purpose of any such no circumstances shall MOODY Shave any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to,any error (negligent or otherwise)

5 Or other circumstance or contingency within or outside the control of MOODY Sor any of its directors, officers, employees or agents inconnection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct,indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY Sis advised in advance of thepossibility of such damages, resulting from the use of or inability to use, any such information. The credit ratings , if any, constituting part of the information containedherein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities.

6 NOWARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OFANY SUCH Rating OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY S IN ANY FORM OR MANNER Rating or otheropinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user mustaccordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it mayconsider purchasing, holding or selling. Pursuant to Section 17(b) of the Securities Act of 1933, MOODY Shereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MOODY Shave, prior to assignment of any Rating , agreed to pay toMOODY Sfor appraisal and Rating services rendered by it fees ranging from $1,000 to $1,500,000.

7 PRINTED IN FalkensteinEditorCrystal CarrafielloAssociate AnalystAndrew BoralProduction AssociateJohn TzanosOur goal for RiskCalc is to develop a benchmark that will facilitate transparency for what hastraditionally been a very opaque asset class - commercial loans. Transparency, in turn, willfacilitate better risk management, capital allocation, loan pricing, and is currently being used within Moody's to support its ratings of loan learn more, please visit s Rating Methodology 3 Table of ContentsSummary ..1 Introduction ..9 What We Will Cover ..10 Section I: The Current Credit Risk Toolbox ..10 Applications ..11 Consumer Bureau Scores ..11 Business Report Scores ..12 Public Firm Models ..12 Agency ratings ..13 Hazard Models.

8 13 Exposure Models ..13 Portfolio Models ..13 Where RiskCalc Fits In ..13 Section II: Past Studies And Current Theory Of Private Firm Default ..14 Empirical Wor k ..14 Theory Of Default Prediction: Comparing The Approached ..15 Traditional Credit Analysis: Human Judgement ..15 Structural Models ..17 The Merton Model and KMV ..18 The Gambler's Ruin ..18 Equity Value vs. Cash Flow Measures: Is One Better? ..19 Nonstructural Models ..19 Appendix 2 ..21 Merton Model and Gambler's Ruin ..21 Section III: Data ..22 Public Company Data: Moody's Default Database and Compustat ..22 Private Company Data: Moody's Credit Research Database (CRD) ..23 Data Composition ..23 Geographic Distribution of Data ..24 Industrial Composition of Data.

9 24 Financial Statement Quality ..25 Sales Size ..26 Financial Institutions' Internal Risk ratings ..26 Summary of Databases ..27 Section IV: Univariate Ratios As Predictors Of Default: The Variable Selection Process ..27 The Forward Selection Process ..28 Statistical Power and Default Frequency Graphs ..30 Profitability Ratios ..32 Leverage Ratios ..34 Size ..35 Liquidity Ratios ..36 Activity Ratios ..37 Sales Growth ..37 Growth vs. Levels ..38 Means vs. Levels ..40 Audit Quality ..40 Risk Factors We Do Not Use ..41 Conclusion ..42 Appendix 4A ..42 Calibration and Power ..42 Power and Default Frequency ..44 Testing the Need for Recalibration ..46 Section V: Similarities And Differences Between Public And Private Companies.

10 46 Distribution of Ratios ..47 Public/Private Default Rates By Ratio ..49 Ratios and ratings ..52 Section VI: Transformations And Functional Form ..54 Transformations ..54 Functional Forms ..57 Appendix 6A: Transformations Of Input Ratios ..59 Appendix 6B: RiskCalc Schema ..60 Input Fields ..60 Ratios ..61 Ratio Calculation ..61 Intermediate Output - The Unadjusted Probability of Default ..62 Final Output: 1-Year DP & 5-Year DP ..62 Mapping into Moody's Rating Symbols ..62 Supplemental Information ..62An Example of Relative Contributions ..63 Section VII: Mapping To Default Rates And Moody's ratings ..63 Definitions Of Default ..63 Prediction Horizon ..64 Default Rate And Moody's Mapping ..64 Moody's Mapping Preliminaries.