Example: tourism industry

The Fokker-Planck Equation 1 Introduction

2 Class of Fokker-Planck Equations For my current research in stochastic di erential equations arising in statistical mechanics [8] and the scope of the work that is the focus of this paper [9], we study the class of SDE of the form

Tags:

Information

Domain:

Source:

Link to this page:

Documents from same domain

Chapter 12 Section 5 Lines and Planes in Space

www.math.wisc.eduExample 2 (a) Find parametric equations for the line through (5,1,0) that is perpendicular to the plane 2x − y + z = 1 A normal vector to the plane is:

College Algebra - Department of Mathematics

www.math.wisc.eduCollege Algebra Version p 3 = 1:7320508075688772::: by Carl Stitz, Ph.D. Jeff Zeager, Ph.D. Lakeland Community College Lorain County Community College Modified by Joel Robbin and Mike Schroeder University of Wisconsin, Madison June 29, 2010. ... 3 Linear and Quadratic Functions157

FACULTY AND ACADEMIC STAFF REQUEST TO BE ABSENT

www.math.wisc.eduundergraduate classes due to hardship on students; colleague coverage (faculty or instructional academic staff, but not graduate assistants) is the preferred method, give names. Absence approved by department chair or program director:

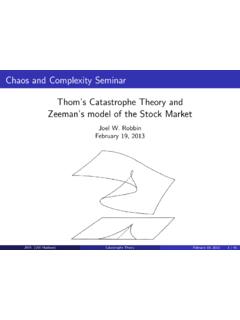

Joel W. Robbin February 19, 2013

www.math.wisc.eduJoel W. Robbin February 19, 2013 JWR (UW Madison) Catastrophe Theory February 19, 2013 1 / 45. The two best things I learned at college. ... Catastrophe theory is a method for describing the evolution of forms in nature. It was invented by Ren´e Thom in the 1960’s. Thom expounded the philosophy

Some analysis problems 1. R - UW-Madison Department of ...

www.math.wisc.eduSome analysis problems 1 1. Let fbe a continuous function on Rand let for n= 1,2,..., Fn(x) = Z x 0 (x− t)n−1f(t)dt. Prove that Fn is ntimes differentiable, and prove a simple formula for its n-th derivative. 2. Let ... P cn converges and P ...

MATH 221 FIRST SEMESTER CALCULUS - Department of Mathematics

www.math.wisc.eduIn modern abstract mathematics a collection of real numbers (or any other kind of mathematical objects) is called a set. Below are some examples of sets of real numbers.

Some Linear Algebra Notes - Department of Mathematics

www.math.wisc.eduDef 2.1 An mxn, matrix is said to be in reduced row echelon form if it satis es the following ... For the matrix A= 2 4 1 1 1 0 3 3 4 1 1 10 4 6 4 2 14 3 5. Find (a) a row-echelon form ... The uniqueness proof is involved, see Ho man and Kunze, Linear Algebra, 2nd ed. Note: the row echelon form of a matrix …

Notes 3 : Modes of convergence

www.math.wisc.eduLecture 3: Modes of convergence 6 Before we give the proofs of these theorems, we discuss further applications of Markov’s inequality and the Borel-Cantelli lemmas.

MATH 221 FIRST SEMESTER CALCULUS - Department of …

www.math.wisc.edu7 VIII. Applications of the integral 125 57. Areas between graphs 125 Exercises 125 58. Cavalieri’s principle and volumes of solids 126 58.1. Example – Volume of a pyramid 126

Related documents

Analysis of Multiscale Methods for Stochastic Di erential ...

web.math.princeton.eduAnalysis of Multiscale Methods for Stochastic Di erential Equations WEINAN E ... ERIC VANDEN-EIJNDEN Courant Institute Abstract We analyze a class of numerical schemes proposed in [25] for stochastic di erential equations with multiple time-scales. Both advective and di usive time-scales are con- ... in the limit of " ! 0 is a stochastic di ...

Numerical Solution of Stochastic Di erential Equations in ...

math.gmu.eduNumerical Solution of Stochastic Di erential Equations in Finance 3 where t i= t i t i 1 and t i 1 t0i t i.Similarly, the Ito integral is the limit Z d c f(t) dW t= lim t !0 Xn i=1

Chapter 4 Stochastic di erential equations

bass.math.uconn.eduChapter 4 Stochastic di↵erential equations 4.1 Poisson point processes Poisson point processes are random measures that are related to Poisson processes. Poisson point processes are also useful in the study of excursions, even excursions of a continuous process such as Brownian motion, and they

Approximation of Stochastic Partial Di erential Equations ...

qiye.mysite.syr.edudimensional problems or in complex domains – even for deterministic partial di erential equations. The kernel-based approximation method (meshfree approximation method [4, 11, 21]) is a relatively new numerical tool for the solutions of high-dimensional problems.

1 Stochastic di⁄erential equations - unipi.it

users.dma.unipi.itIndeed it happens that there are relevant examples of stochastic equations where solutions exist which are not B-adapted. This is the origin of the following de–nitions.

Stochastic Di erential Equations - users.jyu.fi

users.jyu.fiOne goal of the lecture is to study stochastic di erential equations (SDE’s). So let us start with a (hopefully) motivating example: Assume that X t is the share price of a company at time t 0 where we assume without loss of generality that X 0:= 1. To get an idea of the dynamics of X let us

Stochastic Di erential Equations and Integrating Factor

ijnaa.semnan.ac.irStochastic and deterministic di erential equations are fundamentals for the modeling in science, en- gineering and mathematical nance. As the computational power increases, it becomes feasible to

Numerical solution of second-order stochastic di erential ...

jlta.iauctb.ac.irstochastic di erential equation [16], to solve second-order stochastic di erential equation By rst-order stochastic linear system equation which has been mentioned in …

Stochastic Di⁄erential Equations Exercises - HEC Montréal

neumann.hec.caStochastic Di⁄erential Equations Exercises Exercise 11.1. The stochastic process C t = C 0e Wt: t 0; r 0 0 represents the exchange rate evolution, that is C t is the time t value in the domestic currency of one unit of the foreign currency fW t: t 0g is a standard Brownian motion.

Stochastic Difierential Equations - Jagiellonian University

th.if.uj.edu.pllem in terms of stochastic difierential equations, and we apply the results of Chapters VII and VIII to show that the problem can be reduced to solving the (deterministic) Hamilton-Jacobi-Bellman equation.

Related search queries

Of Multiscale Methods for Stochastic Di erential, Of Multiscale Methods for Stochastic Di erential Equations, For stochastic di erential equations, Stochastic di, Numerical Solution of Stochastic Di erential Equations, Chapter 4 Stochastic di erential equations, Chapter 4 Stochastic di↵erential equations, Approximation of Stochastic Partial Di erential Equations, Di erential equations, 1 Stochastic di⁄erential equations, Stochastic equations, Stochastic di erential equations, Stochastic Di erential Equations and Integrating Factor, Stochastic, Stochastic di erential, Stochastic Di⁄erential Equations Exercises, Stochastic difierential equations