Akaike

Found 7 free book(s)

The Journal of Medical Investigation

medical.med.tokushima-u.ac.jpKenichi Aihara Masashi Akaike Kokichi Arisawa Itsuro Endo Kiyoshi Fukui Makoto Funaki Satoshi Goto Akihiro Haga Mari Haku Yasuhiro Hamada Masafumi Harada

セブン&アイ・ホールディングス 東海地方に初のショッピングモールを出店

www.itoyokado.co.jp4 プライムツリー赤池の「施設概要」 【施設名称】 正式名称:primetree akaike(プライムツリー赤池) 【所在地】 日進赤池箕ノ手土地区画整理事業地内11街区

Selecting Variables in Multiple Regression - Statpower

www.statpower.netSelecting Variables in Multiple Regression 1 Introduction 2 The Problem with Redundancy Collinearity and Variances of Beta Estimates 3 Detecting and Dealing with Redundancy 4 Classic Selection Procedures The Akaike Information Criterion (AIC) The Bayesian Information Criterion(BIC)

1 The rugarch package - Booth School of Business

faculty.chicagobooth.edu1.4 Model speci cation of the rugarch package To specify a univariate GARCH model in the rugarc package, one uses the command ugarchspec. See below:

Interpreting Eviews Regression output E270 ; April 2, 1999

mlovell.web.wesleyan.eduInterpreting Eviews Regression output E270 ; April 2, 1999 The following Eviews output was generated with LS HHSNTR C LHUR PDOT LS // Dependent Variable is HHSNTR

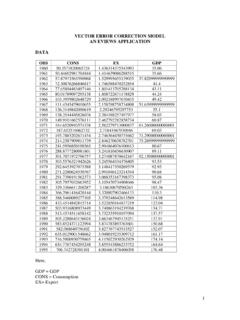

VECTOR ERROR CORRECTION MODEL AN EVIEWS APPLICATION DATA

www.sayedhossain.com11 DECISION: Above ADF operation reveals that GDP is staionary at second difference. So we will use second differenced data of GDP as VAR or VECM model requires stationary data.

Title stata.com nbreg postestimation — Postestimation ...

www.stata.comTitle stata.com nbreg postestimation — Postestimation tools for nbreg and gnbreg DescriptionSyntax for predictMenu for predictOptions for predict Remarks and examplesMethods and formulasAlso see