Transcription of Corporate credit ratings: a quick guide

1 45 Treasurer sCompanionCapitalmarketsandfundingCorpor atecreditratings:aquickguideKristaSantos ,DebtAdvisoryRothschild,LondonTel: it s sim pl est form , a cred it ratingis a fo rmal,inde pe nde ntopin ion of a borrower s abilityto serviceits deb t e maj or ity of ra tingsare publiclydisclosed(th oughnotalw ay s, as we will co me on to later)and ar e used by deb tin ve sto rs in the ir in vestment appraisalprocess(wh er e thera tin g is applie d to a spe cific debt instrument), alt hou gh th eyare al so us ed by cred itorsandoth er par ties fo rund ersta nd ing an en tity screditprofile(wh er e a mor egene ra l ent it y creditratingmaybe issued).Fro m aborr ower sperspective,a cre dit rat in g is ge neral ly are quire ment of publicbon d issuance(cor por ate or highyi eld ) and certainloanstructure s (withins tit utional le nder s)and thu s provides acce ss to a widerran ge of le nde rs anddeb t pro altern ativeca tegory of cred it referencesis thoseprov ide d by Dun n & Brad street, Experian and ot hers.

2 Inaddi tio n to bein g use d by tr ade cr ed itorsan d otherco un ter pa rties,D&B sco res are usedin calcu la ting the UKpen sion reg ula tor s PP F lev y, althoughtheyten d not to beuse d by debt in vestorsan d so are not considere d fur ther inthis guid ed it ra ting s are predomina ntly providedby thr ee mainin de pen de nt ra ting age ncies,namely;St an da rd & Poor s(S& P) , Moo dy s InvestorServices (Moody s), and FitchIB CA(Fit ch) , although the re are th ough the ag encies adoptdifferent ratingsca les, thereis eq uiv ale nce acro ss the scaleswhichfacilit at es comparisonsuc h tha t a Baa1rating(for example)fro m Moody s isequ iva le nt to a BBB+ratingfrom S&P and BBB + fro m Fitch .Th e full ra ting scale s are shownin es torsals o us e a br oadcategorisationof issuers as in ve stm ent grade (Ba a3/BBB-/BBB-and ab ove ) or non-investme nt gra de (aka speculativegrade,junk,highyield beingBa1 /BB+/BB+andbelow).

3 An investmentgraderat ing is importantfor certainborrowersto ensurefullmarketaccess(as someinvestorsare prohibitedfrominv esti ng in su b-i nve stm en t grade deb t), ac hie vin gflex ib le/attractivecove nantsand te rms on debtissues,and insomecas es for the prestigevaluein frontof competitors,cus tomers and sup to req uire greateroperatingand financialre strictionsand n the bondmarkets shu t for severalweekspostLehman, eventhe stronge st investmentgradecompaniescouldnot issuebonds, far less BBBsand reopen,theydid so gradually, opening first tois suersat the top endof the ratingspe ctrumand the neventually movingdowntowardsthe evena AA or A ratingshouldnot be seenas a guaranteeof ,in the currenteconomicclimateit remainschallengin g for non -in vestmentgradecompaniesto is sue debtdue to investors re ducedrisk app etite,An importantexte nsionto the conceptof a borroweroran is sue s creditratingis the ratingoutlook(positive,stable,ne gativeor developing)

4 ,whichis a directionalevaluationofwherethe ratingis likelyto addition,certainentitiessubjectto announcedor expe ctedmajorcorporate eve nts (typicallyaroundM&A)can be placedoncredit-watchpen dingoutcomeof the event,and in somecircumstancesthe agencywill give a viewaboutwhatwouldhappento the ratinglooksnot just at probabilityof default ,but also los s givendefault .Thisis particularlyimp ortantfor non-investme nt gradeissues,wherethe presenceof creditenhancements(assetbacking,security ,covenants,priorityran king)or weak ne sse s (c on tra ctu al or stru ctu ralsub ordination,absenceof securityor covenants)can lead toindividual issuesbeing n otchedup or notcheddown relativeto otherissuesby the sameborrowinggrouporoverallcorporatecre dit ratingto reflecta lowerexpectationof recoveryin the eventof a e ratingagenciesuse broadlysimilarmethodologiesinarrivingat theircreditratingdetermination,althought heyoperateindependentlyof eachotherand so differencesinapproach and ratingoutcomemayexistin certaininstancesThe ra ti ng age nci es distinguish bet weenrati ng sh or t-ter m (<365day s) andlong -te rm (1+ ye ar )

5 Obl ig at ion s, ow ing to the dif fer ent inv estm entdy nam ics of th e di ffe rent investor ge ner al, th ere is little value inha vi ng a sho rt- te rm rati ng unlessissuingcommer cia l pape r and suc hra ti ng is in th e top two ca tego ries, as it is only rea lly use d in the (short-te rm) commerc ial pa per mar ket wh ic h re quire s minim um P2/A-1/F1ra ti ng s. Inve stor s, cr edi tors and otherinterested pa rties te nd to look toa bor rowe r s lo ng -termcreditrat ing as a gen er al me asu re ofcreditwo rth ines d fo r ce rtain secto rs or products,notwithstandingide nticalinf orm cie s providean over viewof theirde tail ed ratingmethodologieson theirwebsites,but inge ne ra l the an alys is wil l focus on two broadareas: Business Risk :Eva lua tio n of stren gths/weaknesses of theop era ti onsof the entity,incl udi ng: mark et positi on ,geo gr ap hi c diversification,sect orst rengths orwe aknes ses, ma rket cyclicality, and compet itiv e dy is ap proachallowsbusinessesto be compare d aga instea ch ot heran d relativest reng th/w ea knes s to beide ntified.

6 Fin anci al Ri sk:Eva lua ti on of the fina ncialfle xib ility of th een tity, including: totalsa les andprofitability mea su re s,ma rgin s, growthexpectations,liquidity,fundingdiv er sityand finan cial for the heartof this ana lysis is cre ditra tio an alysis,whichis usedto quan tita tiv ely positioncom panie s of similar business risk againsteachot he e additional considerationfor the age nciesis the so ve reig n cei ling , whichcan serveto cap at cou ntry ratinglev el the Fore ign Curr encyCredit Rating of a highcreditcorp ora te with jur isd ict ion and prim ary operations in a lo we rcre dit coun try. The agen cies upda ted theirmethodologyin20 05 /6 to reflect percei vedlowerli keli hoodthatago ver nme nt defau lt wou ld be acco mpaniedby a moregen er al moratoriumonfor eign-curr encypay ments(following expansio n of internationalca pitalmarkets),butsuch ins tancestendto be restrictedto the largerplayerswithi n the in frastructure,naturalresources,and to a certa inex tent area of FinancialRisk analysisis oftendistilled(especiallyfor a well knowncompanyin a widelyratedsector)downtothe analysis of a certainnum be r of key cred it numerousadjustmentsthat can be made,andmanyadjustmentsare madeon a sector or evencompanyspecificbasis,thereare a handfulof mainruleswhenitcomesto creditratioana lysis: Deb t adj us tment s.

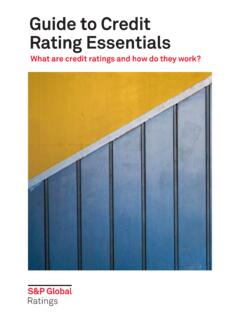

7 The age nc ies typ ica lly cap ita li seope rat ing le ase s and also treat debt-l ike fi nancialoblig ations(suchas post retirementdeficits)as debtwhenarrivingat AdjustedNet (or Tota l) Debt. Fun ds From Oper at ions :The agenciestendto preferFFObased metricsto EBITDA basedmetricsas FFOis a closerprox y to EBITDA less cashinterest and tax, althoughprecisecalculationscan varysignificantlyfromsuchcrudeguides. Re tained Ca shf low/FreeOpera tingCa shflow:TheseareFFO variants(RCFbeingFFOless dividends,FOCF beingTreasurer sCompanionCapitalmarketsandfundingFigure 1: TheratingsstructureAaaAAAAAAAa1AA+AA+Aa2 AAAAAa3AA AA A1A+A+A2 AAA3A A Baa1 BBB+BBB+Baa2 BBBBBBBaa3 BBB BBB Ba1BB+BB+Ba2 BBBBBa3BB BB B1B+B+B2 BBB3B B CaaCCCCCCCaCCCCCCCDDP rime1 Prime2 Prime3 Not primeA 1+A 1A 2A 3 BCDF1+F1F2F3 BCDINVESTMENTGRADENON-INVESTMENTGRADEHIG HESTLOWESTSo urce : Th e As soc iati on of Cor pora te Tr eas urersMOODY SS&PFITCHL ongtermShorttermLongtermShorttermLongter mShortterm47FF O les s cap ex).

8 Operatingleaseadjustments:Le ases are capitalisedon thebala nce she et typically by adjustingrepo rted debt andass et s by the presentvalu e of lease f actorme thod by whic h annualleas e ex pens e ismu lt ip lied by a factorrefle cti ng the averagelife of le asedass et s is also often use d. The im plicit le ase interestisad de d bac k to interest exp enseand EBI TDA . Thedi ffe ren ce be tweenthe averagefirst year minimumleasepa ym ents and the implie d interestexpense,the lea sede preci ation expense , is tr eatedas capexand is addedback to FFO. Hybridbonds:partial equitytreatment for certainqua lifyingde bt ins truments, with level (25%/50%/75%)dependingon le ve l of subordination, maturity,replacement languageand cou pon de ferra l. Bo rrowersissue hy br ids (straightorcon ve rtib le) to sup port (or eve n reach)a desiredcreditra ting , redu cing (or eve n eliminating) the need for hou gh the above can get you muchof the way towardsre plica tin g the publishedcreditratios,it is oftendifficulttore plica te the analy sis exa ctly withoutexplicitgu idancefromthe ra tin g ag encie s.

9 This guidanceis so methingthat is notal wa ys fo rthcoming, bu t in the contextof a transparentre lat io ns hip is some thin g we wouldencouragetre sp on sibi lity for dea ling with the ratin g agencies will usuallylie with the co rpora te tre asure r (or occasionally the fina ncedire ctor dire ct).In orde r to deal effectiv ely with the ratingagencies, it isimp orta nt to un derstand cle arly both how the ratingisde term in ed, an d also its positioning relativeto its en and re gu lar dia loguewith the agen cies, togetherwitha clea r un derstanding of the financialadju stme nts theyem plo y to arriveat the creditratio s, will thereforegreatlyfacil itate a comp an y s und ers tan ding of its ownratin ghe adr oom,risks an d mitiga tre as urer with a go od grasp of how the agenciesana lysebo th hi s businessrisk and fin ancialrisk for their creditwill bebe tter positioned to un derstand the lik ely reactionof theag encie s to chan ge s in op er atingperformance (mark etweak ne ss , in cre ase d comp eti tio n) or corporateevents(a cqu is itions,divestitures and div idends).

10 On e particularare a to focus on is cred it ratio an alysis,asacc ura te re plicationof the pre cise ad justmentsthe agenciesus e will ma ke the qualita tive aspectof the analysisastran spa re nt as bin ed with guidanceonra ti o exp ectations, the abilityto accur ately replicatethe ratingag ency adju stme nts wil l give th e treasurera usefu l too l toan ticip ate the age ncies lik ely re actionto va rious sce narios(s uch as determining the maxim um spe cial divid end tha t canbe ma de witho ut je opard ising a certainrating).It is he lp ful whe n deali ng with the age ncies to presentin ama nn er th at is im medi ately com parablewith their ownan alys is (and even sha re the mode l), whilethe pro visionofcons is tent reliableinformation and the developmentofpr ofessio nal relat ion shi p with an alyst s wil l sign ific antly supp ortcredibility of projections,forecastsand corporateaction.