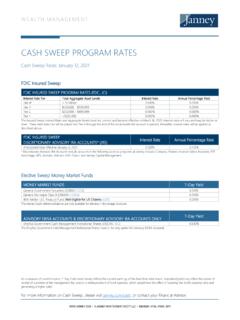

Transcription of 2016 Guide to Complex Debt Reporting - Janney …

1 THE HIGHEST STANDARD OF SUCCESS IN FINANCIAL RELATIONSHIPSWWW. Janney montgomery scott LLC MEMBER: NYSE, FINRA, SIPCREF. 170121 2016 Guide TO Complex debt Reporting PAGE 12016 Guide to Complex debt ReportingTax Year 2016 marks the start of the final phase of the Cost Basis Legislation ( CBL ). This phase requires brokers to report cost basis and annual income adjustments for Complex debt . The CBL was first introduced in 2008 and required incremental increases to the amount of cost basis and income adjustment information reported annually to the IRS by agents such as Janney . Complex debt instruments purchased or acquired before 2016 will remain noncovered, meaning Janney will not report the basis or adjustment information on those shares to the IRS, however clients will still be able to see any information we have on their Consolidated 1099 IS CONSIDERED Complex debt ?

2 Per the IRS, Complex debt for tax Reporting purposes includes debt instruments in the following categories: A debt instrument that provides for more than one rate of stated interest (for example, a debt instrument with stepped interest rates) A convertible debt instrument (that is, one that permits the holder to convert it into stock of the issuer) A stripped bond or coupon A debt instrument that requires payment of either interest or principal in a currency other than the dollar A debt instrument that entitles the holder to a tax credit (or credits) A debt instrument that provides for a payment-in-kind feature A debt instrument issued by a issuer A debt instrument for which the terms of the instrument aren t reasonably available to the broker within 90 days of the date the debt instrument was acquired by the customer A debt instrument issued as part of an investment unit (for example, a debt instrument issued with an option, security, or other property) A debt instrument evidenced by a physical certificate unless such certificate is held (whether directly or through a nominee, agent, or subsidiary) by a securities depository or by a clearing organization described in Treas.

3 Reg. (b)(18) A contingent-payment debt instrument A variable-rate debt instrument An inflation-indexed debt instrument (for example, a Treasury Inflation-Protected Security)If you have any questions on assets that do not fit into the above categories, or if you are uncertain if a certain asset qualifies, please see Treas. Reg. (n)(3) for the specific requirements to determine if a debt instrument is a covered security beginning in 2016 . HOW THIS CHANGE AFFECTS YOUR 1099 FORM:Form 1099 will now show cost basis information and adjustments for Complex debt in a reportable section. In previous years, the majority of this information was shown on your 1099 form, but were not provided to the IRS. Those remaining pieces will now move to a Reportable section on the 1099 form. For example, a position of an asset classified as Complex debt which has an acquisition date of 01/01/ 2016 or later and was sold or disposed of in the 2016 tax year will now report under SHORT TERM TRANSACTIONS FOR COVERED TAX LOTS (or LONG TERM TRANSACTIONS FOR COVERED TAX LOTS if they were inherited as a result of a death occurring in 2016 ).

4 WWW. Janney montgomery scott LLC MEMBER: NYSE, FINRA, SIPC REF. 170121 2016 Guide TO Complex debt Reporting PAGE 2 WHERE IS INTEREST INCOME REPORTED?Interest income is reported on the 1099-INT section of the Consolidated 1099 form, as shown on the right. The summary of interest income in the applicable account is found on page 2 of the Consolidated 1099 form with detailed information shown by CUSIP and/or symbol in the later section labeled Detail for Interest Income. In addition, tax-exempt interest details are shown in the following section, labeled Detail for Tax-Exempt Interest. See below for of29 INTEREST INCOME2016 1099-INT*1- Interest income (not included in line 3)38, Early withdrawal Interest on US Savings Bonds & Treasury Federal income tax Investment country or US possession:6- Foreign tax Tax-exempt interest (includes line 9)26, Specified private activity bond interest (AMT)2, Market discount (covered lots) Bond premium (taxable, categorized below) Non Treasury obligations (covered lots) Treasury obligations (covered lots) Bond premium on tax-exempt bonds (categorized below) Tax-exempt obligations (covered lots) Tax-exempt private activity obligations (AMT, covered lots) Tax-exempt and tax credit bond CUSIP numberSee detailThe following amounts of tax-exempt original issue discount are not reported to the IRS.

5 Tax-exempt original issue discount (includes the line below) Tax-exempt original issue discount private activity bonds (AMT) TO INTEREST AND ORIGINAL ISSUE DISCOUNTThe amounts in this section are not reported to the IRS. They are presented here for yourreference when preparing your income tax return(s).Taxable accrued interest paid13, accrued Treasury interest accrued interest accrued interest paid (AMT) accrued nonqualified interest accrued nonqualified interest accrued nonqualified interest paid (AMT) interest5, nonqualified nonqualified interest (AMT) shortfall on contingent payment debt1, premium- Non Treasury obligations (noncovered lots) premium- Treasury obligations (noncovered lots) premium- Tax-exempt obligations (noncovered lots) premium- Tax-exempt obligations (AMT, noncovered lots) premium- Non Treasury obligations (noncovered lots) premium- Treasury obligations (noncovered lots) premium- Tax-exempt obligations (all lots) premium- Tax-exempt obligations (AMT, all lots) discount (noncovered lots) ISSUE DISCOUNT SUMMARYUse bond-by-bond details from theForm 1099-OIDpage(s)

6 To determine amounts of OriginalIssue Discount income for your income tax return(s). The amounts shown in this section are foryour reference when preparing your income tax return(s).Original issue discount for 20153, periodic withdrawal income tax discount (covered lots) premium (total for covered lots, categorized below) Non Treasury Treasury issue discount on Treasury TAX WITHHELDUse the details of theState Tax W ithholdingpage(s) to determine the appropriate amounts foryour income tax return(s). The amounts shown in this section are for your total total total total total , FEES, EXPENSES AND EXPENDITURESThe amounts in this section are not reported to the IRS. They are presented here for yourreference when preparing your income tax return(s).Other Receipts & Reconciliations- Partnership distributions24, Receipts & Reconciliations- Foreign tax paid- Receipts & Reconciliations- Return of Receipts & Reconciliations- Deferred income Receipts & Reconciliations- Deemed Receipts & Reconciliations- Income accrual- Receipts & Reconciliations- Basis Receipts & Reconciliations- Foreign tax pd beyond & Expenses- Margin interest18, & Expenses- Dividends paid on short & Expenses- Interest paid on short & Expenses- Non reportable distribution & Expenses- Other & Expenses- Severance & Expenses- Organizational & Expenses- Miscellaneous & Expenses- Tax-exempt investment Exchange Gains & Losses- Foreign currency * This is important tax information and is being furnished to the Internal Revenue Service.

7 If you are required to file a return, a negligence penalty or other sanction may be imposed on youif this income is taxable and the IRS determines that it has not been montgomery scott LLCS ummary Information(continued)Page18 of29 Janney montgomery scott LLCD etail for Interest IncomeThis section of your tax information statement contains the payment level detail of taxable interest and associated bond premium. Market discount will be shown here only if you have elected torecognize it currently rather than at the time of sale or maturity. Bond premium and market discount for covered tax lots are totaled on Form 1099-INT and reported to the IRS. For noncovered tax lots,they are totaled in the Adjustments to Interest and Original Issue Discount and are not reported to the provide a complete picture of activity for each investment, we also include here nonreportable transactions such as accrued interest paid on purchases and payment or receipt of nonqualifiedinterest.

8 Other amounts, such as federal, state and foreign tax withheld and investment expenses are shown as negative amounts but do not net against the reportable income amounts shown as Agency interest may be exempt from state tax. You may wish to consult with your tax advisor, the IRS or your state tax authority regarding the proper descriptionCUSIP and/or symbolDateAmountTransaction typeNotesEQUITY04/09/15-1, interest pd04/15/151, , , , interest pd: Interest Income:12345678902/28 interest0302/28 excess- contingent debt0305/29 interest0305/29 excess- contingent debt0308/29 interest0308/29 excess- contingent debt0311/29 interest0311/29 excess- contingent debt03 Interest Income:3, , interest06/28 interest06/28 shortfall- contingent debt09/28 interest09/28 shortfall- contingent debt10/19 accrued interest recd2, , , interest pd04/01/151, , , Income:Interest shortfall- contingent debt :123456789 Accrued interest pd:Interest Income.

9 3, of29 Janney montgomery scott LLCD etail for Tax-Exempt InterestThis section of your tax information statement contains the payment level detail of tax-exempt interest and associated bond premium. Market discount will be shown here only if you have elected torecognize it currently rather than at the time of sale or maturity. Market discount income is NOT federally tax-exempt. Bond premium and market discount for covered tax lots are totaled on Form1099-INT and reported to the IRS. For noncovered tax lots, they are totaled in the Adjustments to Interest and Original Issue Discount and are not reported to the provide a complete picture of activity for each investment, we also include here nonreportable transactions such as accrued interest paid on purchases and payment or receipt of nonqualifiedinterest. Other amounts, such as federal and state tax withheld and investment expenses are shown as negative amounts but do not net against the reportable income and adjustment totals at the end of this section are categorized by your state of residence, US possessions and other states.

10 Note that income is shown as in state only if it is exempt fromstate descriptionCUSIP and/or symbolStateDateAmountTransaction TypeNotesEQUITYAA03/31 accr interest recdEQUITYAA06/01/151, interest08/28 accr interest recd1, 123456789 Tax-Exempt Interest: 123456789AA06/17 accrued interest pd12/01 interestTax-exempt accrued interest interest12/01 interest1, interest12/01 interest1, , interest AMT10/01/151, interest AMT2, , interest07/01/151, interest123456789 Tax-Exempt Interest: 123456789 Tax-Exempt Interest: 123456789 Tax-Exempt Interest: 123456789 Tax-Exempt Interest:2, Janney montgomery scott LLC MEMBER: NYSE, FINRA, SIPC REF. 170121 2016 Guide TO Complex debt Reporting PAGE 3 WHAT IS OID?Original issue discount (OID). OID is a form of interest. It is the excess of a debt instrument s stated redemption price at maturity over its issue price (acquisition price for a stripped bond or coupon).