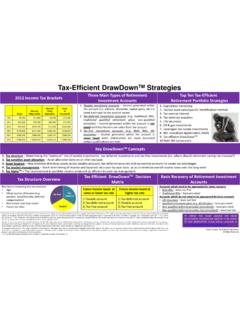

Transcription of TRADITIONAL IRA DISTRIBUTION FLOWCHART

1 TRADITIONAL IRA DISTRIBUTION FLOWCHART . Is the spouse more Is the IRA Yes Is the IRA Yes Is the spouse the Yes than 10 years younger than IRA Yes Calculate RMDs using Joint and Last owner age owner? Educational info: Email to be owner living? sole beneficiary? Survivor Table added to our newsletter or for information regarding No No No licensing agreements, seminars and speeches. Visit No for additional educational materials. RMDs not Calculate RMDs Who is the Beneficiary? yet required using Uniform Lifetime Table Are there Spouse Trust Charity Estate Non-Spousal Individual multiple (See PLR 201208039 for in-kind Beneficiary beneficiaries? distributions from estate). Did spouse Does the trust qualify Yes No perform a as a designated RMDs based No spousal rollover?

2 Beneficiary? See PLRs Did IRA owner die on remaining No Were separate accounts RMDs based on life 200228025 and before his required created by Dec. 31st of year life expectancy expectancy 200235039. beginning date? of decedent following the year of IRA of beneficiary Yes No Yes as of death owner's death? based on Single Inherited Yes based on Life Table*. Yes No IRA - See Five-Year Rule Single Life Inherited Were separate accounts Table Rollover - (or six years if IRA RMDs based on RMDs based on life IRA - Spousal created by Dec. 31st of year owner died after Take RMD for life expectancy of expectancy of oldest Beneficiary following the year of IRA 2003 but before year of each beneficiary beneficiary based on chart on next owner's death?)

3 2010 - see IRC Sec. death, if based on Single Single Life Table *. page. 401(a)(9)(H)(ii)(II)). applicable, Yes No Life Table *. then go to Possible life expectancy of each beneficiary*. step one under Single Life Table if separate trust Life expectancy of oldest trust *Or the owner's life expectancy if the treating beneficiary based on Single owner is younger than the oldest trust shares in existence on the date that a person Life Table* beneficiary and the IRA owner died survivor as dies and the BDF specifically names each new owner. separate share as beneficiary. See PLR after his/her required beginning date. 2012 Keebler Tax & Wealth Education 200537044 All Rights Reserved. Last Updated: 03/09/12. For discussion purposes only.

4 This chart does not represent tax, accounting, or legal advice and is intended to provide generic and general information about the laws applicable to retirement benefits. The individual taxpayer should rely on his or her own advisors. The author, his firm or anyone forwarding or reproducing this work have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. Pursuant to the rules of professional conduct set forth in Circular 230, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the IRS, and it cannot be used by any taxpayer for such purpose.

5 No one, without our express prior written permission, may use or refer to anything in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party. Inherited IRA - Spousal Beneficiary Single Life Table Age Multiple Age Multiple Age Multiple Owner Spouse may defer required distributions until the year the owner would have reached age 70 . Thereafter, Dies 0 37 74 RMDs are calculated based upon spouse's life expectancy by referencing her attained age for the year of Before 1 38 75 DISTRIBUTION under the Single Life Table . For each succeeding year, this process is repeated. (RECALC'D). RBD 2 39 76 RMD for year of death must be taken based upon decedent's life expectancy factor under the Uniform Lifetime 3 40 77 Table.

6 Thereafter, the applicable DISTRIBUTION period is the longer of: (1) the surviving spouse's life expectancy 4 41 78 based on the Single Life Table using the surviving spouse's birthday for each DISTRIBUTION calendar year after the 5 42 79 Owner calendar year of the employee's death up through the calendar year of the spouse's death. For each 6 43 80 Dies succeeding year, this process is repeated. (RECALC'D); or (2) the life expectancy of the deceased spouse under 7 44 81 After the Single Life Table using the age of the deceased spouse as of his or her birthday in the year of death, 8 45 82 RBD. whereby in subsequent years, this factor is reduced by one. 9 46 83 10 47 84 11 48 85 12 49 86 Non-Designated Beneficiary 13 50 87 Death 14 51 88 Entire balance must be distributed no later than December 31st of the fifth anniversary year of the decedent's Before 15 52 89 death.

7 However, consider (if possible) the potential to cash out non-individual beneficiaries, or segregate RBD 16 53 90 interests. PLR required. 17 54 91 Death RMD must be taken for year of decedent's death based upon decedent's age in year of death based on the 18 55 92 After Uniform Lifetime Table. For the first DISTRIBUTION year, determine factor be referencing the owner's age in year 19 56 93 RBD of death and reduce by one. This factor is then reduced by one for each succeeding year. 20 57 94 21 58 95 22 59 96 UNIFORM LIFETIME TABLE 23 60 97 Attained Age in year of Applicable Divisor under Attained Age in year of Applicable Divisor under 24 61 98 DISTRIBUTION Final Regulations DISTRIBUTION Final Regulations 25 62 99 70 93 26 63 100 71 94 27 64 101 72 95 96 28 65 102 73 74 97 29 66 103 75 98 30 67 104 76 99 100 31 68 105 77 78 101 32 69 106 79 102 33 70 107 80 103 104 34 71 108 81 82 105 35 72 109 83 106 36 73 110 84 107 85 108 111 86 109 87 110 88 111 Educational info: Email 89 112 to be 90 113 added to our newsletter or for information regarding 91 114 licensing agreements, seminars and speeches.

8 Visit 92 115 and older for additional 2012 Keebler Tax & Wealth Education educational materials. All Rights Reserved. Last Updated: 03/09/12. For discussion purposes only. This chart does not represent tax, accounting, or legal advice and is intended to provide generic and general information about the laws applicable to retirement benefits. The individual taxpayer should rely on his or her own advisors. The author, his firm or anyone forwarding or reproducing this work have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. Pursuant to the rules of professional conduct set forth in Circular 230, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the IRS, and it cannot be used by any taxpayer for such purpose.

9 No one, without our express prior written permission, may use or refer to anything in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.