Transcription of 2015 State of the Industry - Boating Industry

1 State of the Industry 2015 State of the Industry 2015 Nov. 15- 18 in Orlando Visit for more information. * Vicky Yu, NMMA * Peter Houseworth, Info- Link * Noel Lais, Spader Business Management Our panelists today Available at 2015 Market Data Book NMMA Industry UPDATE Vicky Yu Director, Industry Statistics and Research 6 TODAY S TALKING POINTS State of the Industry Headwinds Opportunity 7 TTRRAADDIITTIIOONNAALL PPOOWWEERRBBOOAATT RREETTAAIILL UUNNIITT SSAALLEESS 100 200 300 400 500 600 1980 1985 1990 1995 2000 2005 2010 2015 Projected UNITS 1980s Recession Asian Financial Crisis Desert Storm Iraq War Great Recession 911 Source.

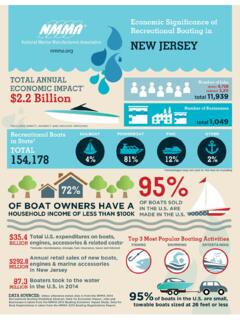

2 NMMA, SSI State of the Industry 8 RETAIL SALES REVENUE source: NMMA $- $1 $2 $3 Outboard boats Outboard engines Boat trailers Inboard skiboats Inboard cruisers Sterndrive boats Canoes Kayaks Inflatables Personal watercraft Jet boats Sailboats Billions 2013 2014 State of the Industry 9 2014 UNIT SALES GROWTH SINCE RECESSION source: SSI State of the Industry 73% 68% 46% 38% 35% 23% 22% 19% 18% 16% 16% 11% 0% 10 GROWTH IN 2015 source: SSI State of the Industry 7/15 YTD YOY Change - Bellwehter Retail Sales 11 0% 10% 20% FL TX MI MN NY NC WI CA LA AL YOY Change Top 10 states 2014 NEW BOAT SPENDING source: NMMA State of the Industry 12 HHOOUUSSIINNGG SSTTAARRTTSS BBOOAATT SSAALLEESS Source.

3 Census Bureau, SSI - 500 1,000 1,500 2,000 2,500 7/1/2001 1/1/2002 7/1/2002 1/1/2003 7/1/2003 1/1/2004 7/1/2004 1/1/2005 7/1/2005 1/1/2006 7/1/2006 1/1/2007 7/1/2007 1/1/2008 7/1/2008 1/1/2009 7/1/2009 1/1/2010 7/1/2010 1/1/2011 7/1/2011 1/1/2012 7/1/2012 1/1/2013 7/1/2013 1/1/ 2014 7/1/ 2014 1/1/ 2015 7/1/ 2015 - 50 100 150 200 250 300 350 Housing Starts, SAAR R12M Retail Powerboat Sales State of the Industry 13 -10 40 90 140 190 240 290 340 390 440 490 Jan-13 Apr Jul Oct Jan-14 Apr Jul Oct Jan-15 Apr Jul (Thousands of Employees) Nonfarm Payrolls Manufacturing 200 MONTHLY CHANGES IN EMPLOYMENT Source: BLS State of the Industry 14 CCIITTYY RREETTAAIILL GGAASS PPRRIICCEESS 8/17/ 2015 , $ $ $ $ $ $ $ $ $ $ $ $ Regular, Conventional Gas Weekly Price Series Max: July 14, 2008, $ Source: EIA State of the Industry 15 CCOONNSSUUMMEERR SSPPEENNDDIINNGG Source: Census Bureau State of the Industry 0% 1% 2% 3% 4% 5% 6% 7% 8% Total Exc.

4 Gas Stations 16 OOUUTTBBOOAARRDD EENNGGIINNEE RREETTAAIILL SSAALLEESS 312 302 276 227 181 179 179 193 209 218 157 $ $ $ $ $ $ $ $ $ $ $ Dollars (Billions) Units (Thousands) Source: NMMA State of the Industry 17 GLOBAL ECONOMY Source: JP Morgan Headwinds 18 STRONG DOLLAR 0% 10% 20% 30% 40% 50% 60% Canada Mexico Australia Europe Japan Columbia China Brazil New Zealand USD BUYING POWER YOY GROWTH Top Boat Export Markets Source: USITC, XE Headwinds 19 AGING BOATER Source: Info-Link Headwinds <25 25-34 35-44 45-54 55-64 65-74 75+ 0% 5% 10% 15% 20% 25% 30% Age % of All Boat Owners 1997 2013 20 STAGNANT MIDDLE CLASS Source: EPI Headwinds 21 RISING STUDENT DEBT Source: NY Fed Consumer Credit Panel/Equifax Headwinds 22 Job Growth Low gas prices Product Innovation Diversify Targets GROWTH DRIVERS Opportunity All data presented today can be found in the following publications.

5 NMMA 2014 recreational Boating Statistical Abstract NMMA Data Dashboard Vicky Yu - - The Difference Between Guessing and KNOWING State of the Industry August 20, 2015 The Difference Between Guessing and KNOWING New boat sales growth in the mid to high single digits in line with expecta ons The Difference Between Guessing and KNOWING Seeing con nued weakness in the 15 19 category The Difference Between Guessing and KNOWING Weakness is more pronounced among small fiberglass boats The Difference Between Guessing and KNOWING Entry Level Value Buyers 40% 38% 0% 20% 40% 60% 80% 100% Value Buyer All Buyers Entry Level Buyers and

6 Prior Boat Ownership No Yes 58% 55% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Value Buyer All Buyers Prior Purchase Type among Prior Owners PRE- OWNED NEW The Difference Between Guessing and KNOWING Value Buyers Prior Boat Ownership and Propulsion 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% Inboard Jet Outboard PWC Sail Stern Prior Boat Ownership by Propulsion Type Value Buyer All Buyers The Difference Between Guessing and KNOWING Con nued strength in Saltwater Fishing boats The Difference Between Guessing and KNOWING A er years of driving growth, Pontoon boats sales appear to be slowing somewhat The Difference Between Guessing and KNOWING While s ll up YOY in most states , growth has moderated in a number of key states and a few states have shown small declines The Difference Between Guessing and KNOWING The Pontoon distribu on channel is clear for the me being 2015 Spader Business Management, Inc.

7 All rights reserved. Noel Lais, Vice President of Operations State of the Marine Industry Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc.

8 All rights reserved. Marine Dealership Trends YTD Averages May 2015 compared to May 2014 July 2015 compared to July 2014 New Boat Sales + + Used Boat Sales + + New Boat Inventory + + Used Boat Inventory Total Spending + + Net Profit + + Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc. All rights reserved. Fulfilling. Success. 2015 Spader Business Management, Inc.

9 All rights reserved. 2015 Spader Business Management, Inc. All rights reserved. Thank you Questions?