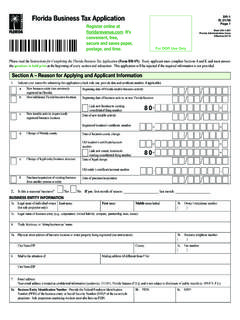

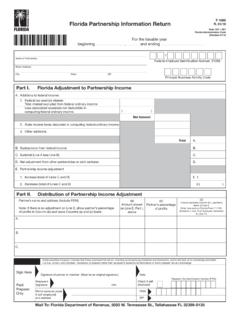

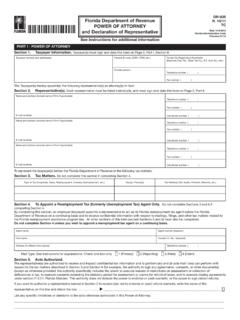

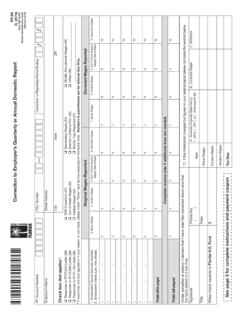

Transcription of The Florida Real Property Appraisal Guidelines

1 The Florida real Property Appraisal Guidelines Adopted in 2002 NOTICE: These Guidelines Are Out-of-Date The existing Florida real Property Appraisal Guidelines were adopted in 2002 and are now out-of-date due to various changes in law. For example, in 2007 the Supreme Court issued a decision holding that Appraisal is an applied science (not an art) and that Appraisal methodology must be reviewed in ad valorem tax valuations. In another example, 2009 changes in sections and , , greatly increased the legal standards for developing, reporting, and reviewing just valuations and also enacted the following additional determinative standards for just valuations: 1) compliance with professionally accepted Appraisal practices; 2) avoidance of arbitrarily different Appraisal practices within groups of comparable Property within the same county; 3) avoidance of superseded case law; and 4) correct application of an appropriate Appraisal methodology. Accordingly, the 2002 Guidelines should not be used as any sort of standard for just valuation development, reporting, or review.

2 The Department has initiated the legal and professional research for updating the Guidelines , which will be done using an open and public process with opportunities for public review and comments. Florida Department of Revenue The Florida real Property Appraisal Guidelines Adopted November 26, 2002 Florida DEPARTMENT OF REVENUE Property TAX ADMINISTRATION PROGRAM TABLE OF CONTENTS INTRODUCTION Overview and Specific Authority Statutory Focus on the Mass Appraisal Process Description of Guidelines Purposes of These Guidelines Intended Users of These Guidelines Intended Uses of These Guidelines Uses for Which These Guidelines Are Not Intended Organization and Content of These Guidelines Sources of Information and Expertise for These Guidelines Other Sources of Appraisal Guidance FOUNDATIONS OF MASS Appraisal IN Florida Legal and Regulatory Foundations Florida Constitution Florida Statutes Florida Administrative Code Florida Case Law The Florida real Property Appraisal Guidelines Comparison of Single- Property Appraisal and Mass Appraisal History and Evolution of Mass Appraisal The Four Forces That Influence real Property Value Legal/Regulatory Forces Physical/Environmental Forces Economic Forces

3 Social Forces Education and Training of Assessment Personnel IMPORTANT DEFINITIONS AND CONCEPTS Important Definitions Ad Valorem Tax Assessment Roll real Property Personal Property Just Value Fair Market Value Market Value Arm s-Length Transaction Distinctions Between Cost, Price, and Value Market Participants Stratification Quality Assurance Relevant Concepts Concept of Fairness in real Property Ad Valorem Taxation Concept of Anticipation Concept of Substitution Concept of Change Concept of real Property Markets Concept of Appraisal Judgment THE MASS Appraisal PROCESS IN Florida Overview Mass Appraisal Systems Computer-Assisted Mass Appraisal Systems Market Variation Between Counties The Annual Just Valuation Cycle for Florida Property Appraisers DEFINING THE MASS Appraisal PROCESS Identification of real Property Regulatory Identification of real Property Administrative Identification of real Property Identification of Property Groups for Mass Appraisal real Property Rights to be Appraised Purpose and Intended Use of the Appraisal Intended Users of the Appraisal Date of Appraisal COLLECTING AND MANAGING MASS Appraisal DATA The Importance of Data Completeness and Accuracy

4 Legal, Physical, and Economic Data Considerations for the Scope of Data Collection General Data Specific Categories of real Property Appraisal Data Collecting and Managing Title Transfer Documents Collecting and Managing Cadastral Mapping Data Collecting and Managing Aerial Photographs Collecting and Managing Regulatory Data Collecting and Managing Data on Physical Characteristics Collecting and Managing Cost and Depreciation Data Collecting and Managing Sale Data Arm s Length Transactions Sale Coding and Reporting Requirements Additional Sale Coding Using Sale Data Separate Maintenance of Sale Characteristics Special Considerations in Sale Data Management Collecting and Managing Income Capitalization Data Accessibility and Confidentiality of Financial Records The Role of Property Owners in Data Collection The Coding of Mass Appraisal Data Quality Assurance for Data Collection and Management Data Collection Manuals Education and Training for

5 Management and Staff Internal Procedural Reviews Internal Quality Audits Data Entry Edits Within CAMA Systems Data Edit Reports From CAMA Systems Exploratory Data Analysis GEOGRAPHIC STRATIFICATION FOR MASS Appraisal Description and Importance Geographic Stratification for Mass Appraisal Market Areas Other Levels of Geographic Stratification Types of Geographic Units Boundaries for Geographic Units Uses of Geographic Stratification in the Mass Appraisal Process EXPLORATORY ANALYSIS OF MASS Appraisal DATA Description and Importance Variation in Applicability The Importance of Coding and Stratification Data Analysis Techniques Measures of Central Tendency Measures of Dispersion One-Variable Profiles, Charts, and Graphs Two-Variable Profiles, Charts, and Graphs Uses of Exploratory Data Analysis CONSIDERATION OF HIGHEST AND BEST USE Overview of Highest and Best Use The Two Components of Highest and Best Use The Tests of Highest and Best Use Market Activity and Highest and Best Use Present Use and Highest and Best Use Changes in Highest and Best Use VALUATION PLANNING Description and Importance Internal Communication Sale Ratio Studies Matching Property Data on Sale Date and Appraisal Date The Importance of Stratification Statistical Indicators in Sale Ratio Studies Sale Ratio Study Applications CONSIDERATION OF VALUATION APPROACHES Overview of Valuation Approaches Considerations for Selecting a Valuation Approach Mass Appraisal Model Structure, Specification.

6 And Calibration LAND VALUATION Land Valuation Overview Stratification for Land Valuation Units of Comparison for Land Valuation Land Market Analysis Factors to Consider in Just Valuations Land Valuation Methods The Sales Comparison Approach to Land Valuation The Abstraction or Extraction Method The Allocation Method The Capitalization of Ground Rent Method The Land Residual Technique Special Considerations in Land Valuation Legal Changes to Land Physical Changes to Land THE COST LESS DEPRECIATION APPROACH Description of the Approach The Importance of Stratification Units of Cost Factors to Consider in Just Valuations Replacement Cost New The Comparative Unit Method The Unit-in-Place Method Published Cost Manuals Application of Replacement Cost New Market Adjustments to Replacement Cost New Description of Accrued Depreciation Actual Age and Effective Age Physical Deterioration Functional Obsolescence External Obsolescence Application of Accrued Depreciation Market Adjustments to Depreciation Tables Land Valuation Just Valuation From the Cost Less Depreciation Approach Quality Assurance in the Cost Less Depreciation Approach THE SALES COMPARISON APPROACH Description of the Approach The Importance of Stratification Units of Comparison Factors to Consider in Just Valuations Applications of the Sales Comparison Approach Relative Comparison Analysis Multiple Regression Analysis Adaptive Estimation Procedure Quality Assurance in the Sales Comparison Approach THE INCOME CAPITALIZATION APPROACH Description of the Approach The Importance of Stratification Units of Comparison for Income and Operating Expenses Factors to Consider in Just Valuations Market Rent and Fee Simple Estate Market Rent and Expense Analysis Income and Operating Expenses Potential Gross Income Vacancy and Collection Loss Effective Gross Income

7 Operating Expenses Reserves for Replacement of Short-Lived Items Net Operating Income, Before and After Reserves Direct Capitalization Overall Capitalization Rates Gross Income Multiplier Method Yield Capitalization Quality Assurance in the Income Capitalization Approach QUALITY ASSURANCE FOR Florida MASS Appraisal The Quality Assurance Process Florida Law, Administrative Rules, and Regulatory Requirements Effective Education and Training Mass Appraisal Data and the Mass Appraisal Process Just Valuation Edits Within CAMA Systems Desk Reviews and Field Reviews Sale Ratio Studies Uses of Sale Ratio Studies Inappropriateness of Selective Reappraisal Matching Property Data on Sale Date and Appraisal Date The Importance of Stratification Graphic Displays of Sale Ratio Study Results Statutory real Property Strata Measures of Appraisal Level in Sale Ratio Studies Adjustment for the First and Eighth Criteria Level of Assessment Measures of Appraisal Uniformity in Sale Ratio Studies Coefficient of Dispersion Price-Related Differential Horizontal Equity Vertical Equity Statistical Indicators for Regulatory Purposes Reconciliation of the Mass Appraisal Evaluating Appraisal Performance for Unsold Property Percent Change in Just Value Methods Unit Just Value Method Taxpayer Feedback INTRODUCTION

8 Overview and Specific Authority. Section 4, Article VII, of the Florida Constitution, requires a just valuation of all real Property for ad valorem taxation, with certain exceptions. Section 1(d), Article VIII, of the Florida Constitution, provides for the voters of each county to elect a Property Appraiser every four years. Florida Property Appraisers have the statutory responsibility to list and appraise all real Property in each county each year for purposes of ad valorem taxation. The Florida Department of Revenue is a state administrative agency with the statutory responsibility of general supervision of the assessment and valuation of real Property for purposes of ad valorem taxation. The functions of Property Appraisers and the Department of Revenue are distinct and separate. Sections (1), (1), and , Florida Statutes, contain a requirement for the Department of Revenue to develop and promulgate real Property Appraisal Guidelines to aid and assist Florida Property Appraisers in the performance of their valuation responsibilities.

9 These statutes describe the specific authority and legislative intent for the development and promulgation of these real Property Appraisal Guidelines , as well as the scope of their legislatively intended use. Section (1), Florida Statutes, states the following: The department shall prepare and maintain a current manual of instructions for Property appraisers and other officials connected with the administration of Property taxes. This manual shall contain all: (a) Rules and regulations. (b) Standard measures of value. (c) Forms and instructions relating to the use of forms and maps. Consistent with section , the standard measures of value shall be adopted in general conformity with the procedures set forth in section , but shall not have the force or effect of such rules and shall be used only to assist tax officers in the assessment of Property as provided by section Section (1), Florida Statutes, states the following: The Department of Revenue shall have general supervision of the assessment and valuation of Property so that all Property will be placed on the tax rolls and shall be valued according to its just valuation, as required by the constitution.

10 It shall also have supervision over tax collection and all other aspects of the administration of such taxes. The supervision of the department shall consist primarily of aiding and assisting county officers in the assessing and collection functions, with particular emphasis on the more technical aspects. In this regard, the department shall conduct schools to upgrade assessment skills of both state and local assessment personnel. Section , Florida Statutes, states the following: In furtherance of the requirement set out in section , the Department of Revenue shall establish and promulgate standard measures of value not inconsistent with those standards 2provided by law, to be used by Property appraisers in all counties, including taxing districts, to aid and assist them in arriving at assessments of all Property . The standard measures of value shall provide Guidelines for the valuation of Property and methods for Property appraisers to employ in arriving at the just valuation of particular types of Property consistent with sections and The standard measures of value shall assist the Property appraiser in the valuation of Property and be deemed prima facie correct, but shall not be deemed to establish the just value of any Property .