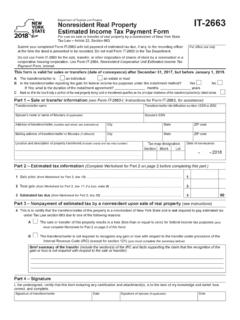

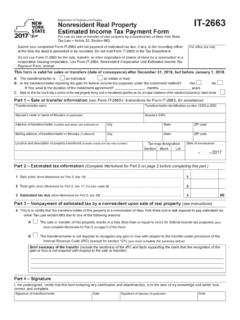

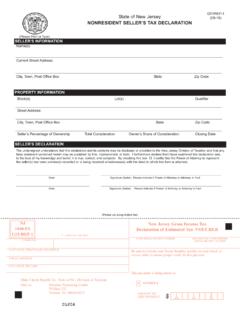

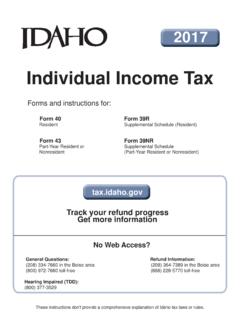

Transcription of 2017 Income Tax Return FORM for Trusts and CT …

1 2017 FORM CT-1041 connecticut Income Tax Return for Trusts and Estates Resident Trusts and Estates nonresident Trusts and Estates Part-Year Resident TrustsThis booklet contains information and instructions about the following forms: Form CT-1041 Schedule CT-1041B Schedule CT-1041C Schedule CT-1041FA Form CT-1041 EXT Form CT-1041ES Schedule CT-1041 K-1 Schedule CT-1041 WHFile Form CT-1041, Form CT-1041 EXT, or Form CT-1041ES using the information is available on the DRS website Department of Revenue Services (DRS) tax information is listed on the back DepositChoose direct deposit for your connecticut Income tax Line 18 - Amount to Be Refunded, on Page CT-1041 can be filed through the connecticut Federal/State Electronic Filing Modernized e-file (MeF) 2 Table of ContentsWhat s New.

2 4 Other Taxes for Which the Trust or Estate May Be Liable .. 5 connecticut Income Tax Withholding .. 5 Controlling Interest Transfer Taxes .. 5 Definitions .. 6 General Information .. 7 How to Get Help .. 7 Forms and Publications .. 7 Where to File .. 7 Modernized e-file (MeF) .. 7 Mailing Addresses for Form CT-1041 .. 7 Who Must File Form CT-1041 .. 7 connecticut Minimum Tax Credit .. 8 connecticut Tax Returns for Individuals .. 8 Tax Returns for Decedents .. 8 Change of Residence of the Grantor of a Revocable Trust .. 8 connecticut Taxable Income for Certain Inter Vivos Trusts .. 8 Fiduciary Adjustment for Lump Sum Distributions .. 8 Sale or Disposition of an Interest in an Entity that Owns Property in connecticut .. 8 How Part-Year Resident Trusts Are Taxed.

3 9 connecticut Income Taxation of Bankruptcy Estates .. 9 connecticut Income Taxation of Debtors Who Are Individuals .. 10 Qualified Funeral Trusts (QFT) .. 10 Composite Return .. 10 Reporting for a Portion of a Resident Trust .. 10 Special Accruals .. 10 Surety Bond in Lieu of Special Accruals .. 11 Taxable Year and Method of Accounting .. 11 When to File Form CT-1041 .. 11 Using the 2017 Form CT-1041 for a Taxable Year Beginning in 2018 .. 11 Extension Requests .. 11 Extension of Time to File .. 11 Extension of Time to Pay .. 12 Payment Options .. 12 Estimated Tax Payments .. 12 Exceptions .. 122018 Estimated Tax Due Dates .. 12 Required Annual Payment .. 13 Guidelines for Banking Institutions .. 13 Annualized Income Installment Method .. 13 Special Rules for Farmers and Fishermen.

4 13 Interest on Underpayment of Estimated Tax .. 13 Filing Form CT-2210 .. 13 Interest and Penalties .. 13 Waiver of Penalty .. 14 Refund Information .. 14 Recordkeeping .. 14 Copies of Returns .. 14 Order in Which to Complete Form CT-1041 and Schedules .. 14 Requirement to Attach Copies of Federal Forms .. 15 Instructions for Form CT-1041 .. 15 Filing Year .. 15 Federal Employer Identification Number (FEIN) 15 Name, FEIN, and Address .. 15 Type of Return .. 15 Resident Status .. 15 Type of Entity .. 15 Rounding Off to Whole Dollars .. 15 Negative Numbers .. 15 Form CT-1041 Quick-File Requirements .. 16 Form CT-1041 Quick-File Line Instructions .. 16 Form CT-1041 Line Instructions .. 16 Who Must Sign the Return .. 18 Paid Preparers Signature.

5 18 Alternative Signature Methods .. 18 Mailing the Return .. 18 Credit for Income Taxes Paid to Qualifying Jurisdictions .. 18 Page 3 Instructions for Worksheet A, Credit for Income Taxes Paid to Qualifying Jurisdiction .. 19 Worksheet A - Credit for Income Taxes Paid to Qualifying Jurisdictions .. 19 Income Tax Credits .. 20 Instructions for Worksheet B, Worksheet for Schedule CT-IT Credit .. 21 Worksheet B - Worksheet for Schedule CT-IT Credit .. 21 connecticut Fiduciary Adjustment ..22 Amount Paid or Set Aside for Charitable Purposes .. 22 Member of a Pass-Through Entity .. 22 Beneficiary of Another Trust or Estate .. 22 Entering Additions and Subtractions .. 22 Instructions for Schedule A .. 23 Additions to Federal Taxable Income ..23 Subtractions From Federal Taxable Income .

6 23 Form CT-1041, Questions A, B, and C ..24 Instructions for Schedule CT-1041B .. 25 Part 1 - Shares of connecticut Fiduciary Adjustment .. 25 Part 2 - Percentage of Resident Noncontingent Beneficiaries .. 25 Instructions for Schedule CT-1041C .. 27 Instructions for Schedule CT-1041FA .. 28 Part 1 - Computation of connecticut Tax of a nonresident Estate or Trust and Part-Year Resident Trust .. 28 Schedule CT-1041FA - Line 4 Worksheet .. 28 Part 2 - Trust or Estate s and Beneficiary s Share of Income From connecticut Sources .. 29 Part 3 - Details of Federal Distributable Net Income and Amounts of Income Derived From or Connected With Sources Within connecticut .. 29 Amended Return .. 31 Page 4 What s NewAngel Investor Tax CreditThe Form CT-AIT, Angel Investor Tax Credit, is now obsolete.

7 You must use Schedule CT-IT Credit to calculate the amount of the Angel Investor Tax Credit you can claim on your Return . If you are claiming the Angel Investor Tax Credit, you must complete Part III of the Schedule CT-IT Waiver RequestsThere is a one year statute of limitations imposed on penalty waiver requests received on or after July 1, 2017. The Commissioner cannot consider a request received more than one year from the date a notice of such penalty was first sent to the taxpayer requesting the waiver. For the taxpayer who self reports the penalty on his or her tax Return , the filing date of such Return is considered the date on which the taxpayer was notified of such penalty. See Policy Statement 2017(6), Requests for Waiver of Civil EntitiesSingle Sales Factor Apportionment and Market-Based Sourcing: For taxable years beginning on or after January 1, 2017, a business, trade, profession, or occupation carried on in connecticut and outside of connecticut must apportion its Income using a single factor gross Income percentage.

8 These multistate businesses are required to utilize market-based sourcing for purposes of determining their gross Income must source receipts from the sales of services and intangible property on a market basis. Receipts from the rental, lease, or license of tangible personal property are sourced according to the location of the property. Receipts from the sale of tangible personal property continue to be sourced based upon the location of the purchaser. Businesses that cannot reasonably determine where their receipts should be sourced under the statutory rules may petition the Commissioner to use an alternate method that reasonably approximates such sourcing of intangible property and tangible personal property are excluded from the apportionment calculation (numerator and denominator) if such property is not held by the business primarily for sale to customers in the ordinary course of the company s trade or not apply the apportionment fraction to Income from the rental of real property or gains or losses from the sale of real property.

9 The entire rental Income from connecticut real property or gain from the sale of the property is allocated to connecticut and the entire amount of any loss from the sale is allocated to connecticut . Rental Income from real property located outside connecticut or any gain or loss from the sale of this property is allocated out of receipts from the sale of tangible personal property are excluded from the sales factor, the net gain (or loss) from such sale should be allocated to the state where the property is located and is not subject to Special Notice 2017(1), Legislative Changes Regarding Single- Sales Factor Apportionment and Market Based of nonresident partner s, shareholder s, or beneficiary s share of Income within ConnecticutEffective for taxable years beginning on or after January 1, 2017, nonresident partners, shareholders, or beneficiaries must determine their share of Income derived from or connected with sources within connecticut according to the statutory apportionment provisions of Conn.

10 Gen. Stat. 12-711, rather than according to Conn. Agencies Regs. 12-711(c)-3 and 12-711(c)-4 to the extent such regulations are inconsistent with the revisions to Conn. Gen. Stat. 12-711(c).Page 5 Other Taxes for Which the Trust or Estate May Be LiableThe following information is a general description of other connecticut taxes for which a trust or estate may be liable. Failure to pay these or any other taxes may subject the trust or estate to civil and criminal Income Tax WithholdingAny trust or estate that maintains an office or transacts business in connecticut (regardless of the location of the payroll department) and is an employer for federal Income tax withholding purposes must withhold connecticut Income tax from connecticut wages as defined in Conn.