Transcription of DRAFT MAY 31, 2012 - International Tax Review

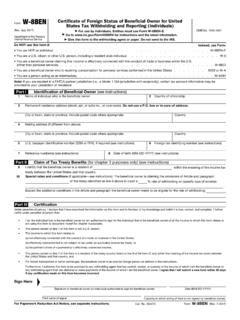

1 Version A, Cycle 3. Form W-8 BEN-E certificate of status of beneficial owner for (Rev. December 2012 ) United States Tax Withholding (Entities) OMB No. 1545-XXXX. Department of the Treasury For use by entities. Individuals must use Form W-8 BEN. Section references are to the Internal Revenue Code. See separate instructions. Give this form to the withholding agent or payer. Do not send to the IRS. Internal Revenue Service Do NOT use this form for: Instead use Form: entity or citizen or resident .. W-9. Any foreign individual .. W-8 BEN (Individual). A foreign individual or entity claiming that income is effectively connected with the conduct of trade or business within the .. W-8 ECI. A foreign partnership, a foreign simple trust, or a foreign grantor trust (see instructions for exceptions).

2 W-8 IMY. A foreign government, International organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, or government of a possession that received effectively connected income or that is claiming the applicability of section(s) 115(2), 501(c), 892, 895, or 1443(b) (see instructions) .. W-8 ECI or W-8 EXP. Note: These entities should use Form W8-BEN-E if they are claiming treaty benefits. Any person acting as an intermediary .. W-8 IMY. Part I Identification of beneficial owner (see instructions). 1 Name of organization that is the beneficial owner 2 Country of incorporation or organization (do not abbreviate). 3 Chapter 3 status (Must check one box only): Corporation Disregarded entity Partnership Simple Trust Grantor trust Complex trust Estate Government Central Bank of Issue Tax-exempt organization Private foundation If you entered disregarded entity, partnership, simple trust, or grantor trust above, is the entity a hybrid making a treaty claim?

3 Yes No DRAFT . 4 Chapter 4 status (Must check one box only unless otherwise indicated) (see instructions for details). Nonparticipating FFI (including limited branch or affiliate of participating FFI) Excepted start-up company. Complete Part XIV. Participating FFI. Complete Part IV. Excepted nonfinancial entity in liquidation or bankruptcy. Complete Part XV. Registered deemed-compliant FFI. Complete Part IV. Excepted hedging/financing center of non-financial group. Complete Part XVI. owner -documented FFI. Complete Part V. Restricted distributor. Complete Part XVII. Certified deemed-compliant nonregistering local bank. Complete Part VI. Territory financial institution. Complete Part XVIII. Certified deemed-compliant non-profit organization. Complete Part VIII. Publicly traded NFFE.

4 Complete Part XIX. Certified deemed-compliant FFI with only low-value accounts. Complete Part IX. Affiliate of publicly traded NFFE. Complete Part XX. MAY 31, 2012 . Foreign government or government of possession. Excepted Territory NFFE. Complete Part XXI. Foreign central bank of issue. Complete Part X. Active NFFE. Complete Part XXII. Entity wholly owned by exempt beneficial owners. Complete Part XII. Passive NFFE. Complete Part XXIII. Excepted nonfinancial holding company. Complete Part XIII. Not applicable (merchant submitting this form solely for purposes of Section 6050W). May check one or both of the following: Certified deemed-compliant retirement plan. Complete Part VII. Exempt retirement funds. Complete Part XI. 5 Permanent residence address (street, apt. or suite no., or rural route).

5 Do not use a box or in-care-of address. City or town, state or province. Include postal code where appropriate. Country (do not abbreviate). 6 Mailing address (if different from above). City or town, state or province. Include postal code where appropriate. Country (do not abbreviate). 7 taxpayer identification number, if required (see instructions) 8 Foreign tax identifying number (see instructions). FFI-EIN QI-EIN EIN. 9 Reference number(s) (see instructions). For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 59689N Form W-8 BEN-E (Rev. 12- 2012 ). Version A, Cycle 3. Form W-8 BEN-E (Rev. 12- 2012 ) Page 2. Part II Claim of Tax Treaty Benefits (if applicable). 10 I certify that (check all that apply). a The beneficial owner is a resident of within the meaning of the income tax treaty between the United States and that country.

6 B The beneficial owner is not an individual, derives the item (or items) of income for which the treaty benefits are claimed, and, if applicable, meets the requirements of the treaty provision dealing with limitation on benefits (see instructions). c The beneficial owner is not an individual, is claiming treaty benefits for dividends received from a foreign corporation or interest from a trade or business of a foreign corporation and meets qualified resident status (see instructions). 11 Special rates and conditions (if applicable see instructions): The beneficial owner is claiming the provisions of Article of the treaty identified on line 10a above to claim a % rate of withholding on (specify type of income): . Explain the reasons the beneficial owner meets the terms of the treaty article: Part III Notional Principal Contracts 12 I have provided or will provide a statement that identifies those notional principal contracts from which the income is not effectively connected with the conduct of a trade or business in the United States.

7 I agree to update this statement as required. Part IV Participating FFI or Registered Deemed-Compliant FFI (see instructions). 13 I certify that the entity identified in Part I: Has the following active FATCA ID ; and Is not submitting this form for payments or an account belonging to a limited branch of an FFI. Part V owner Documented FFI (see instructions). Note. This status only applies if the financial institution or participating FFI to which this form is given has agreed that it will treat the FFI as an owner -documented FFI. In addition, the FFI must make the certifications below. DRAFT . 14a (All owner documented FFIs check here) I certify that the FFI identified in Part I: Does not act as an intermediary;. Does not accept deposits in the ordinary course of a banking or similar business.

8 Does not hold, as a substantial portion of its business, financial assets for the account of others;. Is not an insurance company (or the holding company of an insurance company) that issues or is obligated to make payments with respect to a financial account;. MAY 31, 2012 . Is not affiliated with an entity that accepts deposits in the ordinary course of a banking or similar business, holds, as a substantial portion of its business, financial assets for the account of others, or is an insurance company (or the holding company of an insurance company) that issues or is obligated to make payments with respect to a financial account;. Does not maintain a financial account for any nonparticipating FFI; and Does not issue debt which constitutes a financial account to any person in excess of $50,000.

9 Check box 14b or 14c, whichever applies: b I certify that the FFI identified in Part I: Has provided, or will provide, valid documentation (including waivers), as required, associated with each individual, specified person, owner -documented FFI, exempt beneficial owner , or NFFE that holds, directly or indirectly, an interest in the FFI identified in Part I; and Has provided, or will provide, an FFI owner reporting statement that contains the name, address, TIN (if any), entity tax classification, and the type of documentation provided (when required) for every person that owns an equity interest in the owner documented FFI, each person's Chapter 4 status , the percentage that each owner owns of the owner documented FFI, and any other information the withholding agent requests to fulfill its obligations.

10 C I certify that the FFI identified in Part I: Has provided, or will provide, an auditor's letter, signed within one year of the date of payment, from an independent accounting firm or legal representative with a location in the United States stating that the firm or representative has reviewed the FFI's documentation with respect to all of its owners, that the FFI meets all the requirements to be an owner -documented FFI, and that no owner that owns a direct or indirect interest in the payee is a nonparticipating FFI, specified person, or passive NFFE with any substantial owners. Part VI Certified Deemed-Compliant Nonregistering Local Bank (see instructions). 15 I certify that the FFI identified in Part I: Operates and is licensed solely as a bank in its country of incorporation or organization.