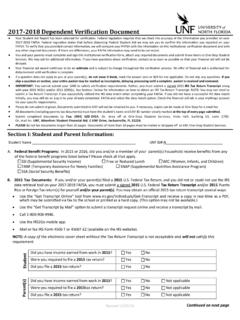

Transcription of 2017 Publication 17 - Internal Revenue Service

1 Userid: CPMS chema: tipxLeadpct: 100%Pt. size: 8 Draft Ok to PrintAH XSL/XMLF ileid: .. ations/P17/ 2017 /A/XML/Cycle02/source(Ini t. & Date) _____Page 1 of 292 17:11 - 12-Dec- 2017 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before of the TreasuryInternal Revenue ServiceTAX GUIDE2017 Get forms and other information faster and easier at: (English) (Espa ol) ( ) ( ) (Pусский) (Ti ngVi t) Your FederalIncome TaxFor IndividualsPublication 17 Catalog Number 10311 GFor use in preparing2017 ReturnsDec 12, 2017 Page 2 of 292 Fileid: .. ations/P17/ 2017 /A/XML/Cycle02/source17:1 1 - 12-Dec- 2017 The type and rule above prints on all proofs including departmental reproduction proofs.

2 MUST be removed before FederalIncome TaxFor IndividualsContentsWhat's One. The Income Tax Exemptions and Withholding and Estimated Two. , Salaries, and Other and Other Income and Plans, Pensions, and Security and Equivalent Railroad Retirement Three. Gains and of of Your Gains and Losses ..118 Part Four. Adjustments to Retirement Arrangements (IRAs).. Five. Standard Deduction and Itemized and Dental Casualty and Theft Expenses and Other Employee Business Benefits for Work-Related on Itemized Six. Figuring Your Taxes and To Figure Your on Unearned Income of Certain and Dependent Care for the Elderly or the Tax Income Credit (EIC).

3 23037 Premium Tax Credit (PTC)..24538 Other Tax Tax Computation Tax Rate Rights as a To Get Tax To explanations and examples in this Publication reflect the interpretation by the Internal Revenue Service (IRS) of:Tax laws enacted by Congress,Treasury regulations, andCourt , the information given does not cover every situation and is not intended to replace the law or change its material in this Publication may be reprinted freely. A citation to Your Federal Income Tax ( 2017 ) would be Publication covers some subjects on which a court may have made a decision more favorable to taxpayers than the interpretation by the IRS.

4 Until these differing interpretations are resolved by higher court decisions or in some other way, this Publication will continue to present the interpretations by the taxpayers have important rights when working with the IRS. These rights are described in Your Rights as a Taxpayer in the back of this of the TreasuryInternal Revenue ServicePage 3 of 292 Fileid: .. ations/P17/ 2017 /A/XML/Cycle02/source17:1 1 - 12-Dec- 2017 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before 's NewThis section summarizes important tax changes that took effect in 2017 . Most of these changes are discussed in more detail throughout this developments.

5 For the latest information about the tax law topics covered in this Publication , such as legislation enacted after it was published, go to the time this Publication went to print, Congress was considering legisla-tion that would do the additional tax relief for those affected by Hurri-cane Harvey, Irma, or Maria, and tax relief for those affec-ted by other 2017 disasters, such as the California certain tax benefits that expired at the end of 2016 and that currently can't be claimed on your 2017 tax return, such as: credit for nonbusi-ness energy property, of the credit for res-idential energy property, deduction for mort-gage insurance premi-ums, of adjusted gross income threshold for de-ducting medical and den-tal expenses, credit for alternative fuel vehicle refueling property, and deduction for tuition and certain other tax !

6 To learn whether this legislation was enacted resulting in changes that affect your 2017 tax return, go to Recent Developments at and theft losses. Dis-aster relief enacted for those im-pacted by Hurricane Harvey, Irma, or Maria includes a provision that modified the calculation of casualty and theft losses. See Pub. 976, Disaster Relief, for more income credit (EIC) and additional child tax credit (ACTC). Disaster relief enacted for those impacted by Hurricane Harvey, Irma, or Maria allows prior year earned income to be elected as 2017 earned income when fig-uring both the 2017 EIC and the 2017 ACTC.

7 See Pub. 976 for more standard deduction. In addition to the annual increase due to inflation adjustments, your 2017 standard deduction is in-creased by any net disaster loss due to Hurricane Harvey, Irma, or Maria. To claim the increased standard deduction, you must file Form 1040. See Pub. 976 for more date of return. File your tax return by April 17, 2018. The due date is April 17, instead of April 15, because of the Emancipation Day holiday in the District of Colum-bia even if you do not live in the District of Columbia. See chap-ter access. To combat iden-tity fraud, the IRS has upgraded its identity verification process for cer-tain self-help tools on To find out what types of information new users will need, go to EIC.

8 You may be able to qualify for the EIC under the rules for taxpayers without a quali-fying child if you have a qualifying child for the EIC who is claimed as a qualifying child by another tax-payer. For more information, see chapter your online account. You must authenticate your iden-tity. To securely log in to your fed-eral tax account, go to View the amount you owe, review 18 months of payment history, access online payment op-tions, and create or modify an on-line payment agreement. You can also access your tax records exemption amount in-creased for certain taxpayers. Your personal exemption is $4,050.

9 But the amount is reduced if your adjusted gross income is more than:$156,900 if married filing sep-arately,$261,500 if single,$287,650 if head of house-hold, or$313,800 if married filing jointly or qualifying widow(er).See chapter on itemized deductions. You may not be able to deduct all of your itemized deductions if your adjusted gross income is more than:$156,900 if married filing sep-arately,$261,500 if single,$287,650 if head of house-hold, or$313,800 if married filing jointly or qualifying widow(er).See chapter mileage rates. The 2017 rate for business use of your vehicle is cents a mile. The 2017 rate for use of your vehicle to get medical care or to move is 17 cents a mile.

10 See Pub. 521, Mov-ing credit. The adoption credit and the exclusion for em-ployer-provided adoption benefits have both increased to $13,570 per eligible child in 2017 . The amount begins to phase out if you have modified adjusted gross in-come (MAGI) in excess of $203,540 and is completely phased out if your MAGI is $243,540 or amount for alterna-tive minimum tax (AMT). The exemption amount for the AMT has increased to $54,300 ($84,500 if married filing jointly or qualifying widow(er); $42,250 if married filing separately).Standard deduction. For 2017 , the standard deduction has in-creased to $6,350 if single; $12,700 if married filing jointly or qualifying widow(er); $6,350 if mar-ried filing separate returns; and $9,350 if head of your return.