Example: quiz answers

Rental properties - Interest expenses

Rental properties Interest expenses If you take out a loan to purchase a rental property, you can claim . the interest charged on that loan, or a portion of the interest, as a deduction. However, the property must be rented, or genuinely available for rent, in the income year for which you claim a deduction. What can you claim? You can claim

Tags:

Information

Domain:

Source:

Link to this page:

Documents from same domain

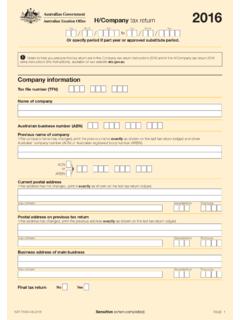

H/Company - Australian Taxation Office

www.ato.gov.auNAT 73004-06.2016 Sensitive (when completed) PAGE 1 H/Company tax return 2016 Notes to help you prepare this tax return are in the Company tax return instructions 2016 and in the H/Company tax return 2016 –

Lodging your tax return - Australian Taxation Office

www.ato.gov.auLodging your tax return https://www.ato.gov.au/Individuals/Lodging-your-tax-return/ Last modified: 29 Jun 2018 QC 32089 Tax returns cover the financial year from 1 …

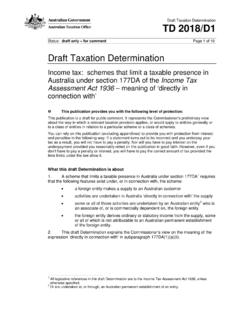

Draft Taxation Determination - ato.gov.au

www.ato.gov.auIdentifying the supply 10. The activities must be referrable to a ‘supply to an Australian customer’. This analysis should be undertaken in light of the nature of the business …

Notification of a deceased person - Australian …

www.ato.gov.auPage 2 Sensitive when completed 6 What was the postal address of the deceased person? Provide the postal address as it was when the person last dealt with the ATO – for example, on the last notice of assessment.

Statement for year ending 30 June - Australian …

www.ato.gov.auHow to complete your PAYG payment summary statement Statement for year ending 30 June The year must be shown as a four digit figure. For example the year ending 30 June 2014 must be shown as ‘2014’ and not ‘14’.

Induction group 4: Funds and USIs Entity ABN Entity …

www.ato.gov.au49633667743 Australian Ethical Retail Superannuation Fund AET0100AU Australian Ethical Retail Superannuation Fund ... 53789980697 OnePath Masterfund MMF2077AU ANZ Smart Choice Pension 53789980697 OnePath Masterfund MMF2076AU ANZ Smart Choice Super

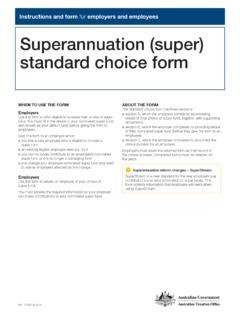

Superannuation (super) standard choice form

www.ato.gov.au2 SUpErANNUATioN (SUpEr) STANdArd ChoiCE form SECTION A: EMPLOYEE TO COMPLETE if you choose your own super fund you will need to obtain current information from your fund to complete items 3 or 4.

How to complete the PAYG payment summary – …

www.ato.gov.au2 HOW TO COMPLETE THE PAYG PAYMENT SUMMARY – INDIVIDUAL NON-BUSINESS FORM HOW TO COMPLETE THIS FORM You must: write each letter in a separate box use a black pen use BLOCK LETTERS.

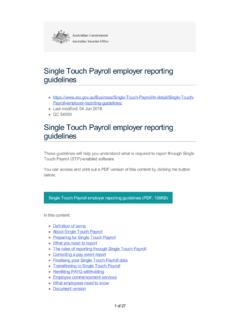

Single Touch Payroll - Secondary

www.ato.gov.auDefinition of terms These terms are referenced throughout the document. Term Definition Digital service provider A digital service provider (DSP) is anyone who develops or delivers digital services

Personal services income for companies, partnerships and ...

www.ato.gov.auPersonal services . income for companies, partnerships and trusts. Guide . for . companies, partnerships and trusts ... PERSONAL SERVICES INCOME FOR COMPANIES, PARTNERSHIPS AND TRUSTS 3. 01. WHAT PERSONAL SERVICES INCOME IS 5 ... through a company, partnership or trust. In many cases, the .

Related documents

Special Attention of: NOTICE H 2021-05

www.hud.govHUD may provide CSPs using CARES Act appropriations only. Amounts made available through other appropriations are not available for this purpose. HUD may cumulatively approve CSPs totaling up to $190 million to Section 8 properties, up to $25 million to properties under the Section 202 program, and up to $9 million for Section 811 properties.

GUIDANCE FOR SEVERE REPETITIVE LOSS PROPERTIES

www.fema.gov(SRL) properties strategy is to eliminate or reduce the damage to residential property and the disruption to life caused by repeated flooding. Approximately 9,000 insured properties have been identified with a high frequency of losses or a high value of claims. As these policies come up for renewal, they will be transferred to

CHAPTER 8. TERMINATION 8-1 Introduction

www.hud.gov5. Assistance is available for the unit. 8-7 Termination of Assistance Related to Establishing Citizenship or Eligible Immigration Status A. Applicability As stated in paragraphs 3-12 F. and 4-31 A., the restriction on assistance to noncitizens applies to all properties covered by this handbook, except the following: 1.

Income and Loss Supplemental - IRS tax forms

www.irs.govinterest as separate properties on line 1 of Schedule E. On lines 3 through 22 for each separate property interest, you must enter your share of the applicable in-come, deduction, or loss. If you have more than three rental re-al estate or royalty properties, complete and attach as many Schedules E as you need to list them. But fill in lines 23a

Like-Kind Exchanges Under IRC Section 1031

www.irs.govTo accomplish a Section 1031 exchange, there must be an exchange of properties. The simplest type of Section 1031 exchange is a simultaneous swap of one property for another. Deferred exchanges are more complex but allow flexibility. They allow you to dispose of property and subsequently acquire one or more other like-kind replacement properties.

$250 PROPERTY TAX DEDUCTION FOR PARTIAL EXEMPTIONS …

www.state.nj.usClaim Form PTD must be filed with your $550,000 but not in excess of $850,000; municipal tax assessor or collector. Additionally, Form PD5, Annual Post-Tax Year Income Statement must be filed with your tax collector each year after initial qualification. PARTIAL EXEMPTIONS FROM REALTY TRANSFER FEE (N.J.S.A. 46:15-10.1)