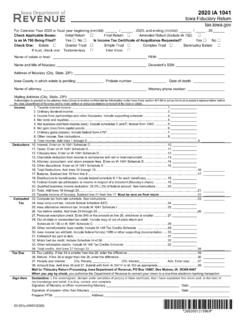

Transcription of 2020 IA 1065 Partnership Return of Income - Iowa

1 2020 ia 1065 partnership return of income Who Must File property, the amount of Income apportioned to Every Partnership deriving Income /loss from real, Iowa is to be based on that portion which the tangible, or intangible property owned within Iowa gross sales made within the state bears to the or from a business carried on within Iowa must file. total gross sales of the Partnership . The sale of The Iowa Partnership form must also be used by tangible personal property occurs in Iowa if the syndicates, pools, joint ventures, limited liability property is shipped or delivered to a point within companies, and other similar entities required to Iowa, regardless of the Freight on Board (FOB). report activities on a federal Partnership Return . point or other conditions of the sale. If the Note: Only partnerships with activity ( Income /loss) Partnership 's distribution includes Income from Iowa sources or which are domiciled in Iowa derived from business other than the are required to file.

2 A non-Iowa Partnership should manufacture or sale of tangible personal not file only because one or more of its partners property, it is to be apportioned to Iowa in the are Iowa residents or because the Partnership is ratio to which the Iowa gross receipts bear to the registered with the Iowa Secretary of State. total gross receipts of the Partnership . The Partnership will provide each partner a copy of Distribution of Partnership Income the IA Schedule K-1, which will show how the A Partnership is not a taxable entity in Iowa, but Iowa portion of the Partnership Income is the members of a Partnership are taxed on their apportioned to each partner. individual shares whether actually distributed to them or not. This pass - through Income is Tax Preference Items reportable on the partner's individual, trust, or If the Partnership had tax preference or corporate tax Return .

3 Alternative minimum tax (AMT) adjustment items, they will be allocated to the partners in the same Individual Partners: If the tax year of a partner ratio as net Income from the Partnership is is different from that of the Partnership , the allocated. The partners may be subject to the distributable share is to be included in the Iowa AMT on the items of tax preference or individual Return for the year in which the tax adjustments allocated to them. year of the Partnership ends. When filing Iowa individual Income tax returns, all partners must Iowa Resident Out-of-State Tax Credit report all Partnership Income that is reportable on 2020 Iowa Acts, House File 2641, Division XVII, the partner's federal Return on the IA 1040. modified the Iowa Out-of-State Tax Credit for tax Modifications may be reported on the Other years beginning on or after January 1, 2020, to adjustments or Other Income lines of the IA allow Iowa residents to claim the credit for certain 1040.

4 In addition, nonresident partners must entity -level Income taxes paid by a pass - through report all Iowa-source Income and adjustments on entity ( Partnership , S corporation, fiduciary) to IA 126, Iowa Nonresident and Part-Year Resident another state, local jurisdiction, or foreign country Credit. Individual Income tax filing requirements on Income also subject to tax in Iowa, but only if are available in the IA 1040 instruction booklet. the partner receives a supplemental schedule These instructions are available on the from the Partnership reporting certain Department website ( ). information. If the Partnership paid entity -level Income tax (including composite Return Income Composite Filing tax) to another state, local jurisdiction, or foreign A Partnership may file an Iowa composite country on the distributive share of the partner's individual Income tax Return and pay any tax due Income also subject to tax in Iowa, provide a on behalf of the nonresident partners who have supplemental schedule to the partner with the IA.

5 No other Iowa Income and meet minimum Income Schedule K-1 that identifies the jurisdiction and requirements. See IA 1040C for further the partner's pro-rata share of the Income , tax information. liability, and tax paid in that jurisdiction. A partner Apportionment of Iowa-Source Income will not be permitted to claim an Out-of-State Tax If a Partnership 's Income is from the Credit on the IA 130 for that Income tax unless manufacture or sale of tangible personal the partner receives that supplemental schedule 41-017a (10/13/2020). from the Partnership and submits a copy with the Fuel Tax Credit IA 1040. If the Partnership does not have a fuel tax refund If the Partnership is itself an owner of another permit or has canceled its refund permit within pass - through entity that paid entity -level Income the first 30 days of the year, a Fuel Tax Credit tax to another state, local jurisdiction, or foreign may be claimed by each partner on his or her country on Income also subject to tax in Iowa, and individual Income tax Return (or by a C.)

6 The Partnership receives a schedule from that corporation if it is a partner). If a Fuel Tax Credit pass - through entity identifying the jurisdiction and is claimed, complete the IA 4136 and include it the Partnership 's pro-rata share of the Income , with the IA 1065. Each partner's share is Income tax liability, and Income tax paid in that recorded in Part III of the partner's IA Schedule jurisdiction, the Partnership may in turn report that K-1. Income tax to its partners on a supplemental Other Tax Credits schedule with the partner's IA Schedule K-1. The Partners may qualify for various tax credits supplemental schedule must identify the passed through to them by the Partnership . The jurisdiction and pass - through entity that paid the Partnership must complete the appropriate Income tax, and the partner's pro-rata share of form(s), where applicable, to compute these that Income , Income tax liability, and Income tax credits (for example: IA 128, IA 137) and include paid.

7 The Partnership may not report this tax to its them with the IA 1065. The Partnership is not partners as described above if the Partnership required to complete an IA 148 Tax Credits does not receive the appropriate schedule from Schedule. Each partner's share of Iowa tax the other pass - through entity . The Partnership credits must be recorded in Part III of the should keep the schedule it received from the partner's IA Schedule K-1 including certificate other pass - through entity because the numbers. Partners must complete the IA 148 to Department may request it of the resident partner claim credits, reporting the Partnership in Part IV. in order to prove the credit claimed on the IA 130. as the pass - through entity . The resident partner is responsible for providing documentation of the out-of-state tax paid by a Time and Place for Filing pass - through entity at the Department's request.

8 The Iowa Partnership Return must be filed on or before the last day of the fourth month following Example: Partnership X earns $2,000 of Income the close of the Partnership 's tax year. For in State A, which imposes an entity -level Income calendar year filers, the due date is April 30, tax directly on the Partnership . Partnership X 2021. There is an automatic 6-month extension pays $100 of Income tax to State A. Partnership of time to file after April 30, 2021. No extension X is owned 50% by Partnership Y, and provides request form is required. Mail returns to Income a schedule to Partnership Y indicating that Y's Tax Return Processing, Iowa Department of pro-rata share of the Income taxed by State A is Revenue, Hoover State Office Building, Des $1,000, and Y's pro-rata share of the Income tax Moines, Iowa 50306-9187.

9 Partners with pass - imposed by and paid to State A is $50. through Income need to review individual, Partnership Y is owned 50% by individual Z, a Limited Liability Company (LLC), trust, or resident of Iowa. Partnership Y provides a corporate Income tax due dates and filing schedule to individual Z indicating that Z's pro- requirements. These instructions are available rata share of Partnership X's Income taxed by on the Department website ( ). State A is $500, and Z's pro-rata share of Partnership X's Income tax imposed by and paid Amended Return to State A is $25. Individual Z may use the Income If an amended federal Return or a federal and tax amounts reported on that schedule in administrative adjustment request was filed, completing Z's IA 130 Iowa Out-of-State Tax the taxpayer must file an amended Iowa Return Credit Schedule, provided that the $500 of and include the IA 102 Amended Return Income identified on the schedule is also reported Schedule.

10 Use the 1065 to file and check the on individual Z's IA 1040 Return and is taxed by Amended Return box. Iowa. 41-017b (10/13/2020). Federal Centralized Partnership Audit Iowa pass - through entity Audits Regime For tax year 2020 and forward, any audit of a Prior to tax year 2018, federal Partnership audit pass - through entity ( Partnership , S corporation, adjustments and tax collection was generally fiduciary) by the Department will be conducted administered at the partner level. For tax years solely at the pass - through entity level through 2018 and forward, the IRS makes audit the entity 's state representative. If a pass - adjustments and generally collects taxes at the through entity is audited by the Department Partnership level for partnerships subject to the resulting in adjustments to Iowa tax liability, the federal centralized Partnership audit regime.